Winter colds have laid the Unknown Family low. We seem to take shifts - Unknown Son and I are in charge of the 11:30 p.m. -2:00 a.m hacking and coughing shift, while Unknown Daughter and Mother handle the mornings. And Unknown Son stayed home from school today with a fever (gee, I wish I could).

I managed to make it through 3 hours of teaching CFA last night, but today should be tougher - I have my regular classes today in the morning (and then another round of CFA teaching tonight). I'll make it through, but it won't be pretty.

After that, I think I'll just pass out for about 12 hours.

Wednesday, January 31, 2007

Sunday, January 28, 2007

Ninja Bunny

This reminds me of the Killer Rabbit from Monty Python's Holy Grail.

HT: Mike Munger

I actually had some serious links to post, but I got the "Blue Screen of Death" and my computer crashed before I could post them. The computer's back up, but Blogger's "recover post" option didn't work. So like Seinfeld, this is all I got.

HT: Mike Munger

I actually had some serious links to post, but I got the "Blue Screen of Death" and my computer crashed before I could post them. The computer's back up, but Blogger's "recover post" option didn't work. So like Seinfeld, this is all I got.

Friday, January 26, 2007

Fama and French Like You've Never Seen Them

The grad students at Dartmouth's Tuck Business School aren't just a bunch of grinds. They also regularly publish a pretty funny spoof "newsletter" calledThe Tuck Profit. In this piece, they "expose" Eugene Fama and Kenneth French:

Read the whole thing here."I hired Ken French in 1990 when he was a driving instructor in Winnetka. Chicago was pressuring me to partner with another researcher; I couldn't stand the idea so I hired a stooge. The man has never contributed a single idea to my research, and yet his name is constantly mentioned in the same breath as mine. On top of it all, the American Finance Association has nominated him as president-elect! That's a travesty and I won't have it."

- Eugene Fama

Washing Your Cat

This last summer the Unknown Wife and Unknown Kids adopted a stray cat. He's outside during the day and stays in the garage (at night) since I'm allergic.

I'm not a cat fan, and I'm not in favor of abusing them.

But this is funny - kind of like a washing machine for cats. My kids thought it was hilarious.

I'm not a cat fan, and I'm not in favor of abusing them.

But this is funny - kind of like a washing machine for cats. My kids thought it was hilarious.

Friday Link Dump

No, I haven't died, gotten sick or fired - just temporarily dropped off the face of the earth due to my having bitten off far more than I can easily chew.

The first week of the semester brought with it a paper deadline, preparing for some topics in the CFA program I'm teaching for the first time, teaching the new modules in a city I had to Amtrack to (twice - I teach for two nights a week), and prepping for and teaching my regular class load.

It wouldn't have been so bad, but of course my computer chose this time to crash Sunday afternoon. Ah well, in any event I'm back, reasonably well rested, and done teaching for the week. And since I did my class prep correctly last semester, I don't have too much to do to get ready for next week. So the rest of today is for catching up on research. Here are some links to keep you busy while I torture some data. Some of it's a bit stale, but I haven't been blogging as much lately and stuff has accumulated in my bloglines account:

The first week of the semester brought with it a paper deadline, preparing for some topics in the CFA program I'm teaching for the first time, teaching the new modules in a city I had to Amtrack to (twice - I teach for two nights a week), and prepping for and teaching my regular class load.

It wouldn't have been so bad, but of course my computer chose this time to crash Sunday afternoon. Ah well, in any event I'm back, reasonably well rested, and done teaching for the week. And since I did my class prep correctly last semester, I don't have too much to do to get ready for next week. So the rest of today is for catching up on research. Here are some links to keep you busy while I torture some data. Some of it's a bit stale, but I haven't been blogging as much lately and stuff has accumulated in my bloglines account:

The New York Times has a good piece on different approaches to "“fundamental indexing."”Enough bloggery - back to work.

The folks at Red Herring examine whether PE and the tech industry (where long-term perspectives and high R&D expenses abound) are a good fit.

TheStreet.com highlights some mutual funds that invest solely in ETFs.

The Capital Spectator is discussingng the odds of a recession.

The Wall Street Journal reports on some cases (maybe a trend) where companies are trying to extract more of the LBO premiums from PE firms. And in a second piece, they discuss "empty voting" - voting with borrowed shares (Larry Ribstein has some very insightful comments here).

Barry Ritholtz at The Big Picture chimes in on The Infallibility of The Markets - as he says, they're not always completelyly right, but they are mostly right.

This week's Carnival of The Capitalists is up at David Maister's blog.

Geoff Considine writes at Seeking Alpha: Outperforming the S&P says nothing about efficient markets. All undergrads should read this - it says what we try to tell them that above benchmark returns could come from higher risk, so you have to correct for risk when measuring returns.

And now, for some non-business items:

Craig Newmark links to two pieces:"13 Things I Wished I Learned in College" and how to think like a genius.

According to CNN, caffeine makes you smarter. That's depressing - it means that without all the coffee I drink I'd be in even worse shape (HT: Mises Economics Blog)

And finally, the weird news of the day (compliments of Hedgefund Guy). This is information I probably didn't really need to know, but having read it, I'm stuck with (and now, so are you).

Monday, January 22, 2007

The Beginning of The Semester - Murphy's Law Edition

I haven't posted much the last few days because of a combination of poor planning, deadlines, and an attack of Murphy's Law. I had a deadline of Monday to submit a paper to a conference (actually, the deadline was last Wednesday, but I know the association people, so I got an extension). In any event, here's what happened:

- The paper was on some aspects of seasoned equity offerings. My coauthor, a graduate student, did the analysis around the date of the actual issue. It should have been done around the date of the ANNOUNCEMENT of the issue. I figured this out on Wednesday, of course.

-So, I ended up redoing his analysis myself. Luckily, I've done a lot of SAS programming (SAS is a statistical software used by a lot of finance academics, among others), so I was able to redo 7 tables of analysis in 4 days.

-I also had to re-write the introduction and results, and conclusions. I should have made him do it, but there was no way he could have gotten it done by the deadline. This isn't bragging -- it's just that I've been doing this a lot longer than he has, I've got a lot of resources (programs to reuse, background in the literature, etc...)

-Classes started today. So, with the paper deadline looming, I figured I'd do my prep on Sunday after the paper was done.

- Of course, that when Murphy struck-- when I opened up my laptop Sunday afternoon (after church), the screen was so faint it was unreadable. Just Damn! I hooked the laptop up to an external monitor, spent about an hour in "Dell Hell" with their technical support folks, and figured out that it was the monitor, and not the processor or hard drive. So, I copied all my data and programs to my office desktop and worked off it.

- I finished the paper around 11:00 Sunday night, and finished my class prep at approximately 1:30 Monday morning (this was after staying at the office until 1:00 the previous night). Then I got up at 6 (thanks to the kids), and taught classes today.

Doing things last minute really makes things interesting. Not easy, but interesting. But everything got done - the paper and the class prep. And I didn't embarrass myself in class (luckily, both classes met before 12:00, so I finished before I ran out of gas).

I even got to have lunch with the Unknown Wife - she just started taking classes in a library science program with a goal of becoming a Media Specialist (what they call school librarians nowadays). Her class ran from 9-12, which is also when mine are done. So we did lunch, paid her tuition bill (the part that wasn't covered by my being a faculty member), bought her textbooks, and set her up on the WebCT system.

But now, it's time for sleep. Then I start all over tomorrow -- I get to finish my prep for the CFA class I teach tomorrow night. I would have done between Wednesday and Friday if the paper hadn't taken all my time, but as they say, "Stuff" happens.

- The paper was on some aspects of seasoned equity offerings. My coauthor, a graduate student, did the analysis around the date of the actual issue. It should have been done around the date of the ANNOUNCEMENT of the issue. I figured this out on Wednesday, of course.

-So, I ended up redoing his analysis myself. Luckily, I've done a lot of SAS programming (SAS is a statistical software used by a lot of finance academics, among others), so I was able to redo 7 tables of analysis in 4 days.

-I also had to re-write the introduction and results, and conclusions. I should have made him do it, but there was no way he could have gotten it done by the deadline. This isn't bragging -- it's just that I've been doing this a lot longer than he has, I've got a lot of resources (programs to reuse, background in the literature, etc...)

-Classes started today. So, with the paper deadline looming, I figured I'd do my prep on Sunday after the paper was done.

- Of course, that when Murphy struck-- when I opened up my laptop Sunday afternoon (after church), the screen was so faint it was unreadable. Just Damn! I hooked the laptop up to an external monitor, spent about an hour in "Dell Hell" with their technical support folks, and figured out that it was the monitor, and not the processor or hard drive. So, I copied all my data and programs to my office desktop and worked off it.

- I finished the paper around 11:00 Sunday night, and finished my class prep at approximately 1:30 Monday morning (this was after staying at the office until 1:00 the previous night). Then I got up at 6 (thanks to the kids), and taught classes today.

Doing things last minute really makes things interesting. Not easy, but interesting. But everything got done - the paper and the class prep. And I didn't embarrass myself in class (luckily, both classes met before 12:00, so I finished before I ran out of gas).

I even got to have lunch with the Unknown Wife - she just started taking classes in a library science program with a goal of becoming a Media Specialist (what they call school librarians nowadays). Her class ran from 9-12, which is also when mine are done. So we did lunch, paid her tuition bill (the part that wasn't covered by my being a faculty member), bought her textbooks, and set her up on the WebCT system.

But now, it's time for sleep. Then I start all over tomorrow -- I get to finish my prep for the CFA class I teach tomorrow night. I would have done between Wednesday and Friday if the paper hadn't taken all my time, but as they say, "Stuff" happens.

Friday, January 19, 2007

Spiders on LSD

You've probably seen photos of webs made by spiders on caffeine, LSD, or cocaine.

Here's a pretty funny YouTube video on the topic (note: may not be work safe)

Here's a pretty funny YouTube video on the topic (note: may not be work safe)

Back Home and In the Office

We made it back from Philly, and Unknown Son is still in remission (yeah!). So that's a huge load off our minds. It's been almost two years since he was "clean", but the quarterly checkups continue, and can still make us a bit nervous.

In any event, it's back in the office to finish up a few things before classes start on Monday. In the meanwhile, here are a few links for your reading pleasure:

In any event, it's back in the office to finish up a few things before classes start on Monday. In the meanwhile, here are a few links for your reading pleasure:

Barry Ritholtz at The Big Picture notes that total margin debt on Wall Street is up 22% since 2005. And he has a chart here.Enough blogging - I have syllabi to write and research to finish.

Professor Andrew Gelman blogs at Statistical Modeling, Causal Inference, and Social Science. He's got a book out titled Data Analysis Using Regression and Multilevel/Hierarchical Models, and it looks promising. The guy knows his stuff.

Lew Sichelman at Marketwatch.com has a good piece on mortgage scams.

Cynthia Koons had a good piece on the market for junk bonds in last Friday's Wall Street Journal. She reports on how lower rates and other features have made LBO companies prefer bank debt over junk bonds as the financing vehicle of choice.

And last but nit least, Joe Carter at Evangelical Outpost has posted the latest installment of his Yak Shaving Razor series.

Tuesday, January 16, 2007

On The Road Again (part 2)

We made it to Philadelphia without incident, but unfortunately the Ronald McDonald House was full. So, we had to stay down the street (we still got a reduced rate - just not as cheap as we would have had at the RMH).

After we checked in to the hotel, we went to the RMH so the kids could unwind for a bit. Then tomorrow, we get his injection. Since I'm working feverishly on a paper to present at the FMA (our national conference), I'll probably camp out for the rest of the day at the UPENN library so I can have access to journals I might need. It's sad - no matter how much time I have, it always seems to come down to the last minute for conference papers. The good news is that we have some nice results, and with luck my Ph.D. student coauthor will have his first "good" conference presentation to put on his vita.

In the meanwhile, here are a few links to keep you busy:

After we checked in to the hotel, we went to the RMH so the kids could unwind for a bit. Then tomorrow, we get his injection. Since I'm working feverishly on a paper to present at the FMA (our national conference), I'll probably camp out for the rest of the day at the UPENN library so I can have access to journals I might need. It's sad - no matter how much time I have, it always seems to come down to the last minute for conference papers. The good news is that we have some nice results, and with luck my Ph.D. student coauthor will have his first "good" conference presentation to put on his vita.

In the meanwhile, here are a few links to keep you busy:

This week's Carnival of the Capitalists is up at Endless Gibberish. I'm pressed for time, so no pick of the week this time.Enough blogging. Time to put the kids to bed.

Mark Hurlburt notes that the January Effect is now 22-2 over the last 24 years.

Irwin Kellner of MarketWatch asks whether the inverted yield curve is bad news of good.

Finally, they had ice in Portland and Seattle. Click here to watch what happens when you mix ice with drivers who aren't used to driving in winter conditions. But don't if you're an insurance agent like my brother - it's too painful.

Monday, January 15, 2007

On The Road Again

As I've mentioned a couple of times before, Unknown Son was diagnosed with Neuroblastoma (a relatively rare form of childhood cancer) on his 4th birthday.

He went into remission in late 2005, but we still go to see his oncologist every 3 months for a checkup (this stuff is known to recur). So, we drive the clan to Philadelphia tomorrow and stay at the Philadephia Ronald McDonald House for a couple of days while we have tests done at Children's of Philadelphia.

There's wireless at the RMH, but I'm also trying to finish up a paper to submit to the Financial Management Association annual conference (the national meeting for pointy-headed academic nerds like me). Of course, the deadline's Wednesday midnight.

This is all to say, blogging will probably be light for the next couple of days.

He went into remission in late 2005, but we still go to see his oncologist every 3 months for a checkup (this stuff is known to recur). So, we drive the clan to Philadelphia tomorrow and stay at the Philadephia Ronald McDonald House for a couple of days while we have tests done at Children's of Philadelphia.

There's wireless at the RMH, but I'm also trying to finish up a paper to submit to the Financial Management Association annual conference (the national meeting for pointy-headed academic nerds like me). Of course, the deadline's Wednesday midnight.

This is all to say, blogging will probably be light for the next couple of days.

I Have a Dream

Since It's Martin Luther King Day, here's a video of MLK's famous "I Have a Dream" speach.

It's 17 minutes long, but worth every minute.

It's 17 minutes long, but worth every minute.

Saturday, January 13, 2007

Salaries For Finance and Business School Faculty

People often wonder what salaries are for Business School faculty. In fact, Google searches on faculty salaries are a common way people stumble across this blog. So, here's a brief rundown on what the current state of affairs is for finance professors. I don't have nearly as much info on other business school disciplines, but I'll link to a study at the bottom of this post with more info for those who are interested.

The good news for those considering a career as a finance professor is that you'll make more than almost any other academic discipline (nowhere near what someone on Wall Street makes, but still not bad). Every year the AACSB (the b-school accrediting organization) does a survey of business school salaries. In the most recent survey (for academic year 2005-2006), the average salaries by rank were as follows:

If you're not an academic, a little explanation is probably in order. First, it's important to understand that once a person is hired, they typically don't experience much in the way of raises (usually a couple percent a year at most) if they stay at their current university. This is because universities realize that once tenured, most faculty won't leave (and take another, likely untenured position) for a few thousand dollars more. So, salaries for faculty hired years ago often lag significantly behind those of new hires. In fact, it's not uncommon for new assistant professors to be hired at salaries that are higher higher than those of existing associate or full professors (this is known as "salary inversion").

Also, in what seems paradoxical, new Ph.D. candidates often have better job prospects than those have been out a few years. This is because they have what's commonly referred to as "option value." Research schools (that generally pay higher salaries than teaching-oriented schools) want candidates that will publish in high-quality journals. A new graduate (particularly from a top school) is probably more likely to publish in top journal than is another candidate who's been out for a few years and has already published a few times in lower-tier journals. The reasoning is that the "seasoned" candidate has revealed his type - his publishing in lower-tier journals signals that the'll likely be a consistent publisher, but not at the journals that the better schools want. As an example, for the 2005-2006 year, while new assistant professors averages $111,000 in salary, new Ph.D.s averaged about $2,000 more. If you asume that new Ph.D.s make up half of the new hires, this implies that non-new Ph.D. hires actually averaged about $109,000 (about $4,000 less than new Ph.D.s).

Because of salary stagnation, the only way a finance prof can keep his salary marked to market is to move schools occasionally. Even if a prof decides not to move, having an offer in hand from another school is often a good way to get a counter-offer from their existing dean. In fact, this has happened to several of my friends in the last few years.

Finally, and this is extremely important, there's a LOT of variation across schools, and average salaries can be misleading. Salaries differ significantly between "teaching" and "research" schools. From conversations I've had recently, a "research" school in the upper tier (not the very top of the heap like Harvard or MIT, but still in the top rank) will likely pay $150k-$160k this year for new faculty. In contrast, lower tier research oriented schools will probably pay more in the $125k-$135k range, while teaching oriented schools will pay nearer to the $90K-$105k range.

There are also differences in "summer support" between teaching and research schools. The salaries I've quoted are "nine-month" salaries (although most faculty elect to have their nine-month salaries spread out over 12 months). Research schools typically pay faculty an additional stipend for the first few years (called "summer support") so that they can take the summer months to concentrate on research. This summer stipend is usually in the range of 1/9 to 2/9 of their nine-month salary. In contrast, teaching schools often pay little or no summer research support.

The numbers I've given are for finance faculty. Typically, accounting professors make similar salaries (in fact, this year they might even be a couple thousand above those for finance profs), while management and marketing professors often make 10-20% less.

Once tenured, many faculty do outside consulting (either for companies or as expert witnesses), which can also be pretty lucrative. ut that's a story for another day.

For a little more info on b-school faculties, here's the promised link to the 2005-2006 AACSB salary survey.

Finally, in case you're interested, I've written a series of posts about the field of academic finance:

The good news for those considering a career as a finance professor is that you'll make more than almost any other academic discipline (nowhere near what someone on Wall Street makes, but still not bad). Every year the AACSB (the b-school accrediting organization) does a survey of business school salaries. In the most recent survey (for academic year 2005-2006), the average salaries by rank were as follows:

Assistant professor - $109,000 ($111,000 for "new hires")

Associate professor - $107,000 ($126,000 for "new hires")

Full professor - $134,000 ($142,000 for "new hires")

New Ph.D. - $113,000

If you're not an academic, a little explanation is probably in order. First, it's important to understand that once a person is hired, they typically don't experience much in the way of raises (usually a couple percent a year at most) if they stay at their current university. This is because universities realize that once tenured, most faculty won't leave (and take another, likely untenured position) for a few thousand dollars more. So, salaries for faculty hired years ago often lag significantly behind those of new hires. In fact, it's not uncommon for new assistant professors to be hired at salaries that are higher higher than those of existing associate or full professors (this is known as "salary inversion").

Also, in what seems paradoxical, new Ph.D. candidates often have better job prospects than those have been out a few years. This is because they have what's commonly referred to as "option value." Research schools (that generally pay higher salaries than teaching-oriented schools) want candidates that will publish in high-quality journals. A new graduate (particularly from a top school) is probably more likely to publish in top journal than is another candidate who's been out for a few years and has already published a few times in lower-tier journals. The reasoning is that the "seasoned" candidate has revealed his type - his publishing in lower-tier journals signals that the'll likely be a consistent publisher, but not at the journals that the better schools want. As an example, for the 2005-2006 year, while new assistant professors averages $111,000 in salary, new Ph.D.s averaged about $2,000 more. If you asume that new Ph.D.s make up half of the new hires, this implies that non-new Ph.D. hires actually averaged about $109,000 (about $4,000 less than new Ph.D.s).

Because of salary stagnation, the only way a finance prof can keep his salary marked to market is to move schools occasionally. Even if a prof decides not to move, having an offer in hand from another school is often a good way to get a counter-offer from their existing dean. In fact, this has happened to several of my friends in the last few years.

Finally, and this is extremely important, there's a LOT of variation across schools, and average salaries can be misleading. Salaries differ significantly between "teaching" and "research" schools. From conversations I've had recently, a "research" school in the upper tier (not the very top of the heap like Harvard or MIT, but still in the top rank) will likely pay $150k-$160k this year for new faculty. In contrast, lower tier research oriented schools will probably pay more in the $125k-$135k range, while teaching oriented schools will pay nearer to the $90K-$105k range.

There are also differences in "summer support" between teaching and research schools. The salaries I've quoted are "nine-month" salaries (although most faculty elect to have their nine-month salaries spread out over 12 months). Research schools typically pay faculty an additional stipend for the first few years (called "summer support") so that they can take the summer months to concentrate on research. This summer stipend is usually in the range of 1/9 to 2/9 of their nine-month salary. In contrast, teaching schools often pay little or no summer research support.

The numbers I've given are for finance faculty. Typically, accounting professors make similar salaries (in fact, this year they might even be a couple thousand above those for finance profs), while management and marketing professors often make 10-20% less.

Once tenured, many faculty do outside consulting (either for companies or as expert witnesses), which can also be pretty lucrative. ut that's a story for another day.

For a little more info on b-school faculties, here's the promised link to the 2005-2006 AACSB salary survey.

Finally, in case you're interested, I've written a series of posts about the field of academic finance:

What's Involved In Getting A Ph.D. In Finance?

What Does A Finance Professor Do All Day? - Part 1 (Teaching)

What Does A Finance Professor Do All Day? - Part 2 (Research)

Classic Bugs Bunny - Kill The Wabbit

A friend of mine just reminded me of how the guys in my dorm would all watch Bugs Bunny on Saturday Mornings. You haven't lived until you've heard a dozen guys singing "Kill The Wabbit."

For those who have no clue what I'm talking about, here's the original Bugs Bunny Wagnerian Opera Spoof.

Yeah, yeah, I know - stop wasting time and get back to work on that paper.

For those who have no clue what I'm talking about, here's the original Bugs Bunny Wagnerian Opera Spoof.

Yeah, yeah, I know - stop wasting time and get back to work on that paper.

If You Knew How To Beat The Market, Would You Tell Anyone?

I'm always amused by financial seminars that offer to tell you (for a fee) how to beat the market with no risk.

The question to ask anyone who tells you they can do this is "If you really knew know how to do this, why would you sell the information?" Why not just use it yourself? After all if it's so profitable, just pay employees to do it for you.

There's a direct parallel in financial economics research. Let's assume that you discover a market anomaly that provides abnormal risk adjusted profits (like, "markets are slow to adjust to positive earnings surprises", or "small firms have abnormally high risk adjusted returns in January").

If you found this, why would you publish it? If you didn't, you could trade on it and make a lot of money. On the other hand, if you publish it, others will start trading on it and the abnormal profits will disappear.

Colby Wright (a Ph.D. student at Florida State) examined this question as part of his dissertation. Here's the abstract of his paper "So You Discovered An Anomaly... Gonna Publish it?":

This basically means that a newer untenured faculty will more likely publish the anomaly because

This also implies that the stuff that tenured senior faculty publish is less likely to be really, really useful in generating abnormal profits.

HT: Hedgefundguy at The Alpha and Omega

Update: Barry Ritholtz makes a good point that I hadn't considered in the comments:

The question to ask anyone who tells you they can do this is "If you really knew know how to do this, why would you sell the information?" Why not just use it yourself? After all if it's so profitable, just pay employees to do it for you.

There's a direct parallel in financial economics research. Let's assume that you discover a market anomaly that provides abnormal risk adjusted profits (like, "markets are slow to adjust to positive earnings surprises", or "small firms have abnormally high risk adjusted returns in January").

If you found this, why would you publish it? If you didn't, you could trade on it and make a lot of money. On the other hand, if you publish it, others will start trading on it and the abnormal profits will disappear.

Colby Wright (a Ph.D. student at Florida State) examined this question as part of his dissertation. Here's the abstract of his paper "So You Discovered An Anomaly... Gonna Publish it?":

A link to the piece is available on SSRN here.If publishing an anomaly leads to the dissipation of its profitability, a notion that has mounting empirical support, then publishing a highly profitable market anomaly seems to be irrational behavior. This paper explores the issue by developing and empirically testing a theory that argues that publishing a market anomaly may, in fact, be rational behavior. The theory predicts that researchers with few (many) publications and lesser (stronger) reputations have the highest (lowest) incentive to publish market anomalies. Employing probit models, simple OLS regressions, and principal component analysis, I show that (a) market anomalies are more likely to be published by researchers with fewer previous publications and who have been in the field for a shorter period of time and (b) the profitability of published market anomalies is inversely related to the common factor spanning the number of publications the author has and the number of years that have elapsed since the professor earned his Ph.D. The empirical results suggest that the probability of publishing an anomaly and the profitability of anomalies that are published are inversely related to the reputation of the authors. These results corroborate the theory that publishing an anomaly is rational behavior for an author trying to establish his or her reputation.

This basically means that a newer untenured faculty will more likely publish the anomaly because

- It builds his reputational capital, thus making it more likely that he'll be able to "trade up" to a better school/higher salary/lower teaching load, more research support, etc...

- It increases his chances of getting tenure

- He really doesn't have the capital to take advantage of the anomaly anyway.

This also implies that the stuff that tenured senior faculty publish is less likely to be really, really useful in generating abnormal profits.

HT: Hedgefundguy at The Alpha and Omega

Update: Barry Ritholtz makes a good point that I hadn't considered in the comments:

...some identified anomalies work better as marketing for products than they do as true trading insight. Consider a well tested investing advantage that provides an annualized 50 or even 150 basis point advantage versus the S&P500 over 10 years. What do you do with that? They may outperform, but any advantage to the discoverer is contingent on attracting significant assets. So you write a book ("Dogs of the Dow"), sell a newsletter (StockTrader's Almanac "Sell in May"). Maybe you can even create a mutual fund firm (Wisdom Tree) for it.

Friday, January 12, 2007

Friday and Home With A Sick Kid

Today started off well - I got up early, swam at the YMCA, and had a good breakfast. The kids got on the school bus, Unknown Wife went to the mall with her sister to do some retail therapy (be afraid -- be very afraid). So I had high hopes of having a very productive day.

Then on the way into my office I got a call from school that Unknown Son was running a fever. And Unknown Wife is now 80 miles away spending money. So, it looks like work from home day.

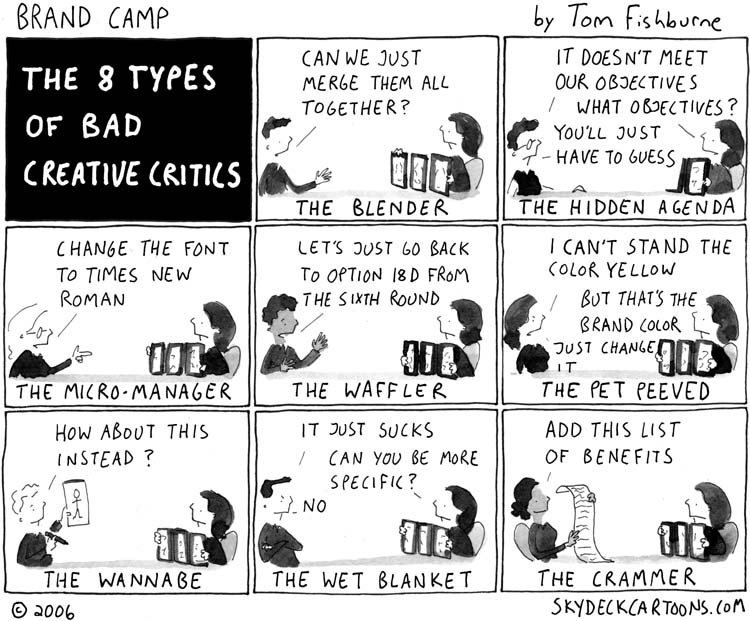

I'll put up some linkes later. In the meantime, vegreville just pointed me to the 8 types of creative critics.

As he says, they have a lot in common with referees at journals.

As he says, they have a lot in common with referees at journals.

Then on the way into my office I got a call from school that Unknown Son was running a fever. And Unknown Wife is now 80 miles away spending money. So, it looks like work from home day.

I'll put up some linkes later. In the meantime, vegreville just pointed me to the 8 types of creative critics.

As he says, they have a lot in common with referees at journals.

As he says, they have a lot in common with referees at journals.

Thursday, January 11, 2007

Thursday Link Dump

It's a good start to the year - I submitted a paper to a journal today. It's been sitting on my desk for too long, but it's done, done, done (at least until it comes back). So now it's on to other things - like getting a paper ready to submit to the Financial Management Association (FMA) conference. This year it's in Orlando, so I definitely want to go.

So while I rewrite my coauthor's first draft, here are some links to keep you busy:

So while I rewrite my coauthor's first draft, here are some links to keep you busy:

The New York Times highlights some rising stars in the field of economics. There are a few that actually do finance.Enough bloggery - back to work.

The next time you want to speak directly to a human being rather than go through the automated phone system, check out this list at gethuman.com

Joe Carter at Evangelical Outpost has the latest installment of his Yak Shaving Razor series.

Richard Shaw at SeekingAlpha.com has a nice chart of the spread between long-term Treasury Bond rates and Treasury Bill rates over the last 80 years.

Finally, the Wall Street Journal discusses how securities firms and making money hand and fist out of sweeps accounts.

A Great Teaching Technique

Here's something I might try this semester:

HT: Newmark's Door

One of my favorite professors in college was a self-confessed liar.Read the whole thing here.

I guess that statement requires a bit of explanation.

The topic of Corporate Finance/Capital Markets is, even within the world of the Dismal Science, a exceptionally dry and boring subject matter, encumbered by complex mathematic models and economic theory.

What made Dr. K memorable was a gimmick he employed that began with his introduction at the beginning of his first class:

"Now I know some of you have already heard of me, but for the benefit of those who are unfamiliar, let me explain how I teach. Between today until the class right before finals, it is my intention to work into each of my lectures ... one lie. Your job, as students, among other things, is to try and catch me in the Lie of the Day."

And thus began our ten-week course.

HT: Newmark's Door

Wednesday, January 10, 2007

Tuesday, January 09, 2007

Tuesday Link Dump

Here are a handful of links for your reading pleasure:

There were two pieces of interest in the New York Times: The first describes how the more attractive compensation arrangements offered by Private Equity firms is allowing them to attract very good CEO-level candidates, and the second highlights the growing prominence of activist investors.I'd post more, but I'm trying to get stuff done before the semester starts.

Here's another neat use of prediction markets -- Intrade (the non-sports betting spinoff of TradeSports) now has a recession contract. It pays off if there's a U.S. recession in 2007, and is currently predicting a 30-35% probability of it happening.

This week's Carnival of the Capitalists is up at the Peersight blog. My pick of the week:Investing While Incompetent - And Blissfully Unaware

Finally, Steven Levitt (and others) explore what factors predict Ph.D. completion and long-term success in the field of economics.

Saturday, January 06, 2007

Sad News For Poor Grad Students The World Over

Momofuku Ando (the inventor of Ramen noodles) died yesterday of a heart attack.

Friday, January 05, 2007

TGIF Link Dump

It's the between-semester break, so Friday isn't such a big deal (unlike when I'm teaching). However, it does signal the end of the school week. So tomorrow is family day.

Lately I've been going to the YMCA to swim and bike before breakfast (it's either that or look for a sponsor to pay for advertising space on my increasingly oversized backside). We have a family membership (it's only $16 more a month than an individual membership) and it's a mere two miles from the Unknown House. So tomorrow, we'll take Unknown Son and Unknown Daughter to go swimming at family swim time.

But before I get back to work, here are some links to keep y'all busy:

Lately I've been going to the YMCA to swim and bike before breakfast (it's either that or look for a sponsor to pay for advertising space on my increasingly oversized backside). We have a family membership (it's only $16 more a month than an individual membership) and it's a mere two miles from the Unknown House. So tomorrow, we'll take Unknown Son and Unknown Daughter to go swimming at family swim time.

But before I get back to work, here are some links to keep y'all busy:

MarketWatch.com has some good tips to help you avoid mortgage fraud.Enough bloggery - back to work.

Craig Newmark links to a site that gives Meanings and Origins of Phrases, Sayings and Idioms. Since I'm a self-confessed "word nerd" and fan of slang, I wasted about a half hour on it today already.

As usual, there are a number of good stories in the Wall Street Journal. In the first (from a couple of days back) we find that The SEC is trying to show that the benefits of their proposed rule requiring 75% independence for the directors of a mutual exceeds its costs. They can't seem to, and they're arguing that it's a limitation of the methodology. Here's a thought - maybe it's because the benefits don't exceed the costs (nope, nah, can't be).

In another WSJ story, Serena Ng reports how there are more and more companies issuing "junk" rated bonds. She argues that it's because of both the increases in LBOs and increases in investors' (like hedge funds) appetites for high-yield debt.

In the third and final WSJ piece, Shefali Anand is examining whether the increasingly large role played by hedge funds is causing distortions in the market for small-cap stocks.

Thursday, January 04, 2007

Thursday Link Dump

Lots to do today, so without further ado, here are today's links:

Marketwatch interviews money manager Ted Aronson about his personal portfolio. He's got an expanded version of the "three fund portfolio" I've mentioned earlier, but it's still all index funds.Enjoy.

Value Blog Review lists some useful blogs for new investors and/or traders.

Michael Covel (Author of Trend Following) has a link to a free PDF of Jesse Livermore's bio Reminiscences of a Stock Operator. It's a great (albeit long) read.

Joe Carter (at Evangelical Outpost) has posted the latest edition of his Yak Saving Razor series of helpful hints and, software, and tools.

Richard Shaw provides some statistics on correlations between asset classes, sectors, and country indexes. Some of the graphs he shhows will make it to next semester's investments class.

Wednesday, January 03, 2007

Wednesday Link Dump - The Wall Street Journal Edition

One of the things I like about the winter semester break is that I have a little more time to keep up on what's happening in the "outside" world.

I'm still trying to get used to the smaller size of the Wall Street Journal, but at least the quality of the stories in it haven't changed. In fact, since I've got a little more time to read it, I've found a lot more good stories in the last few days than usual. So, just call this the "Wall Street Journal" edition of the Link Dump. Note: you need a subscription to read these online, but if you don't have one, you can still buy the paper:

I'm still trying to get used to the smaller size of the Wall Street Journal, but at least the quality of the stories in it haven't changed. In fact, since I've got a little more time to read it, I've found a lot more good stories in the last few days than usual. So, just call this the "Wall Street Journal" edition of the Link Dump. Note: you need a subscription to read these online, but if you don't have one, you can still buy the paper:

First off, there were a number of good articles on the Private Equity world. In today's paper, the article Inside the minds of Kravis & Roberts is worth reading if for no other reason than because Kravis and Roberts were two of the three principals of KKR, which started the whole PE thing off, and still has the record for the largest PE deal ever.That's enough for now - time to do some research.

A related piece (Caveat Investor: IPOs Of Hedge, Equity Funds) discusses how PE & hedge funds firms are starting to issue stock to gain access to "permanent capital".

Finally, in the third piece (from yesterday's Journal), Conglomerate Comparisons compares and contrasts today's PE firms to the conglomerates of the 1960's (like ITT)

A New Way To Rate Stock Tips reports on the increasing popularity of web sites that let investors share ideas online. The latest twist is that some of these sites rate the quality of participants contributions.

In yesterday's Journal, the article titled Investors Riding the Cash Rapids talks about some of the effects that increases in global liquidity is having on stock and bond markets.

And finally, Jonathan Clemens (in his Getting Started column) peels back the curtain on the tricks advisors (both the legitimate and shady) use to get you to sign on the dotted line in Don't Get Hit by the Pitch: How Advisers Manipulate You. A few years back, I read a great book titled The Big Con: The Story of The Confidence Man. It was written by a professor of linguistics that got inside the world of con men in the 1920's and 30's, and it does a fantastic job of detailing the strategies con men use. The same tricks are used today, just with different products and with different delivery methods, like the Internet. So buy it and read it - it's worth the price.

Tuesday, January 02, 2007

Tuesday Link Dump

It's the first "working" day of the New Year, so a Happy New Year to all my readers. Whether you come here regularly or just happened by, I'm glad you're here.

As for the Unknown Household, we pretty much hung around the house for the New Year - we did a lot of family visiting for Christmas, so we decided to stay local for this one. On New Year's day, we got up late and lazed around most of the day - the kids played with Christmas toys, the Unknown Wife read books, and I spent several hours watching the Ultimate Fighting Marathon on Spike TV. Unknown wife can't stand it, but I took taekwondo in high school, played Judo for a couple of years in college, and grew up watching boxing on the Wide World of Sports.

But now, it's back to work. The first order of the day is to clean out all the junk that's been building up in my feed reader. So, here's the first Link Dump of the New Year:

As for the Unknown Household, we pretty much hung around the house for the New Year - we did a lot of family visiting for Christmas, so we decided to stay local for this one. On New Year's day, we got up late and lazed around most of the day - the kids played with Christmas toys, the Unknown Wife read books, and I spent several hours watching the Ultimate Fighting Marathon on Spike TV. Unknown wife can't stand it, but I took taekwondo in high school, played Judo for a couple of years in college, and grew up watching boxing on the Wide World of Sports.

But now, it's back to work. The first order of the day is to clean out all the junk that's been building up in my feed reader. So, here's the first Link Dump of the New Year:

Mark Hulbert of the NY Times highlights an approach to valuing IPOs developed by Andrew Metrick, an extremely smart finance professor at Wharton.And that's all for now folks. Time for some research.

Adam Warner of the Daily Options Report finishes up his series on "option greeks" with a primer on "theta"

Barry Ritholtz at The Big Picture interprets recent data on insider selling.

Now THIS appeals to my inner geek: Avis is provide an option for renters of their cars to make them a mobile Wi-Fi hotspot for $10.95 per day.

And last but not least, this week's Carnival of The Capitalists is up and running at Free Money Finance.

Monday, January 01, 2007

Using Game Theory On Your Kids

At bedtime, the Unknown Kids get a story read to them and it seems like they always want different stories - and I'm only going to read one. We've tried a number of methods for choosing which story to read. Invariably, one child ends up happy and the other doesn't.

So this time, I thought I'd try a little game theory (hey, I studied a lot of this stuff in grad school, and since I'm an empiricist, I don't use it often. And I should get some use out of it). So, here's what we did tonight:

Here's how it played out: In round one, Unknown Daughter choose an American Girl book that Unknown Son had no interest in. Then, for his turn he choose a Sponge Bob book that she had no interest in (big surprise there, so far).

At this point, she said "that's no fair - all you're going to do is choose Sponge Bob books, and I don't like them." Then I took her aside and told her that she could reject his choice if she didn't want it (that's exactly what she did).

At this point, I explained once again that if they both kept saying no, after three rounds, there would be NO story. So, if they used their turns to only chose stories that THEY wanted and that their sibling didn't, their sibling could easily decide that NO story was just as good as a story that they didn't like, and they could end up with NO story at all.

At this point, Unknown Daughter took Unknown Son out into the hallway, and some frantic whispering ensued. About 20 seconds later, they told me that they'd chosen a Disney Story book.

So this episode could show that there's actual benefit to advanced training in Finance and economics.

Or, it could just illustrate why children of academics turn out so different from their peers.

Note: I just noticed a fair bit of traffic coming from a couple of sites that just linked to this post. If you've just wnadered in, welcome. Feel free to stay and look around a bit. If you want to go to the main page, click on the "Financial Rounds" title up at the top. If you want to find out more about the blog, check out the Frequently Asked Questions (FAQ) page. And if your want to subscribe to our RSS feed, there are links on the sidebar.

So this time, I thought I'd try a little game theory (hey, I studied a lot of this stuff in grad school, and since I'm an empiricist, I don't use it often. And I should get some use out of it). So, here's what we did tonight:

- I explained to the kids that that we'd go three "rounds", and if they couldn't agree on a book, by that time. no one would get a story.

- First, we flipped a coin to determine who'd go first. Unknown Daughter (age 6) won.

- For the first round, Unknown Daughter chose a book. Then Unknown Son (age 8) got to either accept the book or reject it. If he rejected it (and he did), he then got to choose one of his own. At this point, Unknown Daughter would get to accept or reject his choice. If she rejected, round one would be over.

- At this point, the choice went back to Unknown Daughter for round two, and she got to choose. And then Unknown Son, and so on.

- The key is that if three rounds went by and a book hadn't been agreed upon, no one got a story.

Here's how it played out: In round one, Unknown Daughter choose an American Girl book that Unknown Son had no interest in. Then, for his turn he choose a Sponge Bob book that she had no interest in (big surprise there, so far).

At this point, she said "that's no fair - all you're going to do is choose Sponge Bob books, and I don't like them." Then I took her aside and told her that she could reject his choice if she didn't want it (that's exactly what she did).

At this point, I explained once again that if they both kept saying no, after three rounds, there would be NO story. So, if they used their turns to only chose stories that THEY wanted and that their sibling didn't, their sibling could easily decide that NO story was just as good as a story that they didn't like, and they could end up with NO story at all.

At this point, Unknown Daughter took Unknown Son out into the hallway, and some frantic whispering ensued. About 20 seconds later, they told me that they'd chosen a Disney Story book.

So this episode could show that there's actual benefit to advanced training in Finance and economics.

Or, it could just illustrate why children of academics turn out so different from their peers.

Note: I just noticed a fair bit of traffic coming from a couple of sites that just linked to this post. If you've just wnadered in, welcome. Feel free to stay and look around a bit. If you want to go to the main page, click on the "Financial Rounds" title up at the top. If you want to find out more about the blog, check out the Frequently Asked Questions (FAQ) page. And if your want to subscribe to our RSS feed, there are links on the sidebar.

Subscribe to:

Posts (Atom)