I get to close out 2008 on hospital room duty with my son. He's doing well - had his breathing tube out yesterday, is eating regular food, and slowly recuperating. He should be moved out of the ICU tomorrow and into a regular room. With some luck, he might be home by Monday the 5th.

The Unknown Wife and Daughter are going to a neighbor's house for a little New Year's cheer (the non-alcoholic kind, since Unknown Wife is expecting), and then home by about 10.

Here's hoping 2009 finds you healthy, prosperous, and happy.

Wednesday, December 31, 2008

Monday, December 29, 2008

Paddy Hirsch Explains Quantitative Easing

Yet another excellent whiteboard talk by Paddy Hirsch, senior editor at Marketplace. In this one, he explains "Quantitative Easing"

Quantitative easing from Marketplace on Vimeo.

Quantitative easing from Marketplace on Vimeo.

How Do You Use Credit Default Swaps (CDS) To Create "Synthetic Debt"?

There's been a lot of talk in recent months about "synthetic debt". I just read a pretty good explanation of synthetics in Felix Salmon's column, so I thought I'd give a brief summary of what it is, how it's used, and why.

First off, let's start with Credit Default Swaps (CDS). A CDS has a lot of similarities to an insurance policy on a bond (it's different in that the holder of the CDS needn't own the underlying bond or even suffer a loss if the bond goes into default).

The buyer (holder) of a CDS will make yearly payments (called the "premium"), which is stated in terms of basis points (a basis point is 1/100 of one percent of the notional amount of the underlying bond). The holder of the CDS gets paid if the bond underlying the CDS goes into default or if other stated events occur (like bankruptcy or a restructuring).

So, how do you use a CDS to create a synthetic bond? here's the example from Salmon's column:

Let's assume that IBM 5-year bonds were yielding 150 basis points over treasuries. In addition, Let' s assume an individual (or portfolio manager) wanted to get exposure to these bonds, but didn't think it was a feasible to buy the bonds in the open market (either there weren't any available, or the market was so thin that he's have to pay too high a bid-ask spread). Here's how he could use CDS to accomplish the same thing:

So why go through all this trouble? One reason might be that there's not enough liquidity in the market for the preferred security (and you'd get beaten up on the bid-ask spread). Another is that there might not be any bonds available in the maturity you want. The CDS market, on the other hand, is very flexible and extremely liquid.

One thing that's interesting about CDS is that (as I mentioned above), you don't have to hold the underlying asset to either buy or write a CDS. As a result, the notional value of CDS written on a particular security can be multiple times the actual amount of the security available.

I know of at least one hedge fund group that bought CDS as a way of betting against housing-sector stocks (particularly home builders). From what i know, they made a ton of money. But CDS can also be used to hedge default risk on securities you already hold in a portfolio.

To read Salmon's column, click here, and to read more about CDS, click here.

First off, let's start with Credit Default Swaps (CDS). A CDS has a lot of similarities to an insurance policy on a bond (it's different in that the holder of the CDS needn't own the underlying bond or even suffer a loss if the bond goes into default).

The buyer (holder) of a CDS will make yearly payments (called the "premium"), which is stated in terms of basis points (a basis point is 1/100 of one percent of the notional amount of the underlying bond). The holder of the CDS gets paid if the bond underlying the CDS goes into default or if other stated events occur (like bankruptcy or a restructuring).

So, how do you use a CDS to create a synthetic bond? here's the example from Salmon's column:

Let's assume that IBM 5-year bonds were yielding 150 basis points over treasuries. In addition, Let' s assume an individual (or portfolio manager) wanted to get exposure to these bonds, but didn't think it was a feasible to buy the bonds in the open market (either there weren't any available, or the market was so thin that he's have to pay too high a bid-ask spread). Here's how he could use CDS to accomplish the same thing:

- First, buy $100,000 of 5-year treasuries and hold them as collateral

- Next, write a 5-year, $100,000 CDS contract

- he's receive the interest on the treasuries, and would get a 150 basis point annual premium on the CDS

So why go through all this trouble? One reason might be that there's not enough liquidity in the market for the preferred security (and you'd get beaten up on the bid-ask spread). Another is that there might not be any bonds available in the maturity you want. The CDS market, on the other hand, is very flexible and extremely liquid.

One thing that's interesting about CDS is that (as I mentioned above), you don't have to hold the underlying asset to either buy or write a CDS. As a result, the notional value of CDS written on a particular security can be multiple times the actual amount of the security available.

I know of at least one hedge fund group that bought CDS as a way of betting against housing-sector stocks (particularly home builders). From what i know, they made a ton of money. But CDS can also be used to hedge default risk on securities you already hold in a portfolio.

To read Salmon's column, click here, and to read more about CDS, click here.

Thursday, December 25, 2008

Bad News

We just got som bad news regarding the Unknown Son. As many of my regular readers already know, he's gone through a lot - he's a two-times cancer survivor.

In 2002 he was diagnosed with Neuroblastoma, a particularly nasty and resistant childhood cancer. After a great deal of chemotherapy, surgery, radiation, more chemotherapy, and experimental treatments (including an autologous (i.e. "self") stem-cell transplant, he went into remission in 2005.

In January of 2008, he was diagnosed with a Wilms' tumor (a kidney tumor), which resulted in the removal of his right kidney and, after more chemo, he was given another clean bill of health this summer.

Now it looks like he has another tumor - in the lower part of his right lung. We just found out about it two days ago as a result of routing follow-up scans. He's scheduled for more surgery this coming Monday (the 29th). He'll get the tumor removed, which will give us the best information as to what exactly it is. He'll probably have about a week-long hospital stay, and we'll then know if this is a recurrence of the Wilms, tumor or something else (it could be a recurrence of his neuroblastoma, but that's unlikely because there was no indication on his latest MIBG scan a couple of weeks back).

So, please keep us in your prayers.

If you're one of my "non-blogosphere" friends (or a regular reader who knows me by my real name) and you want to keep up with what's going on, we maintain a website that we use to keep family and friends abreast of the little guy's treatment. Drop me an email and I'll send it to you in case you want the url.

In 2002 he was diagnosed with Neuroblastoma, a particularly nasty and resistant childhood cancer. After a great deal of chemotherapy, surgery, radiation, more chemotherapy, and experimental treatments (including an autologous (i.e. "self") stem-cell transplant, he went into remission in 2005.

In January of 2008, he was diagnosed with a Wilms' tumor (a kidney tumor), which resulted in the removal of his right kidney and, after more chemo, he was given another clean bill of health this summer.

Now it looks like he has another tumor - in the lower part of his right lung. We just found out about it two days ago as a result of routing follow-up scans. He's scheduled for more surgery this coming Monday (the 29th). He'll get the tumor removed, which will give us the best information as to what exactly it is. He'll probably have about a week-long hospital stay, and we'll then know if this is a recurrence of the Wilms, tumor or something else (it could be a recurrence of his neuroblastoma, but that's unlikely because there was no indication on his latest MIBG scan a couple of weeks back).

So, please keep us in your prayers.

If you're one of my "non-blogosphere" friends (or a regular reader who knows me by my real name) and you want to keep up with what's going on, we maintain a website that we use to keep family and friends abreast of the little guy's treatment. Drop me an email and I'll send it to you in case you want the url.

Monday, December 22, 2008

Window Dressing and Other Mutual Fund Games

What do the following terms have in common?

- Window Dressing

- Painting The Tape/Banging The Close

- Comparison Shopping

- Window dressing happens when the portfolio manager sells off securities just before the end of the reporting period so that they don't show up in the annual (or quarterly) listing o the portfolio's securities.

- Painting the Tape (also called Banging the Close) occurs when a portfolio manager holding a security buys a few additional shares right at the close of business at an inflated price. For example, if he held shares in XYZ Corp on the last day of the reporting period (and it's selling at, say $50), he might put in small orders at a higher price to inflate the the closing price (which is what's reported). Do this for a couple dozen stocks in the portfolio, and the reported performance goes up. Of course, it goes back down the next day, but it looks good on the annual report.

- Comparison Shopping could also be called "benchmark shopping". This refers to the idea that if a fund manager can't beat his benchmark, he just switches to a new benchmark that he can beat.

President Bush and The Military

I try to keep politics mostly out of Financial Rounds because it generally gets people far too worked up. Likewise, I try not to post too much about President Bush. But this piece in the Washington Post caught my eye.

Regardless what else you think about President Bush, he clearly appreciates and honors the role the military plays and the sacrifices those soldiers have made for their country.

For much of the past seven years, President Bush and Vice Prresident Dick Cheney have waged a clandestine operation inside the For much of the past seven years, President Bush and Vice President Dick Cheney White House. It has involved thousands of military personnel, private presidential letters and meetings that were kept off their public calendars or sometimes left the news media in the dark.Read the whole thing here.Their mission: to comfort the families of soldiers who died fighting in Afghanistan and Iraq since the Sept. 11 terrorist attacks and to lift the spirits of those wounded in the service of their country.

Regardless what else you think about President Bush, he clearly appreciates and honors the role the military plays and the sacrifices those soldiers have made for their country.

Saturday, December 20, 2008

Awesome Explanation of the Economic Crisis

I didn't realize this, but every year Harvard's Kennedy School invites new members of congress for a three-day "briefing" by Harvard profs on various topics. This year, Jeff Frankel came up with a graphic explanation of the current economic crisis. Here it is:

Now that's what I call an information-rich slide.

Now that's what I call an information-rich slide.

Thursday, December 18, 2008

Want To See Your Favorite Hedge Fund's Holdings?

You can't see all their holdings. But you can see quite a bit.

Section 13(f) of the Securities Exchange Act of 1934 requires all institutional fund managers with more than $100 million in assets to report their holdings each quarter to the SEC *(within 45 days of the end of the quarter). The hard copies of these filings go back 30 years, but they've been available for free online through the SEC's EDGAR database since 1999. The form name is (not surprisingly) "13F" or "13F-HR". Like many academics, I've used the electronic database of 13F filings put out by Thomson Financial (which has information back to the early 80s on electronic media, runs 5-10 gigabytes, and requires you to have some programming chops to access) in my research. But you can access a fund's data one filing at a time through the Edgar site.

It won't show things like derivatives holdings (at least usually not) or short sales. But if will give you an interesting look at the holding of the big boys. However, you might be looking at a portfolio as much as 45 days old. So, it's best for funds with a long-term (usually value-oriented) approach. As one example, here's the latest filing from Seth Klarman's Baupost Group.

And in case you're interested, here's one for Bernard L. Madoff Investment Securities LLC (I hear the founder has been in the news lately).

HT: World Beta who uses this information in an investment screening tool.

Section 13(f) of the Securities Exchange Act of 1934 requires all institutional fund managers with more than $100 million in assets to report their holdings each quarter to the SEC *(within 45 days of the end of the quarter). The hard copies of these filings go back 30 years, but they've been available for free online through the SEC's EDGAR database since 1999. The form name is (not surprisingly) "13F" or "13F-HR". Like many academics, I've used the electronic database of 13F filings put out by Thomson Financial (which has information back to the early 80s on electronic media, runs 5-10 gigabytes, and requires you to have some programming chops to access) in my research. But you can access a fund's data one filing at a time through the Edgar site.

It won't show things like derivatives holdings (at least usually not) or short sales. But if will give you an interesting look at the holding of the big boys. However, you might be looking at a portfolio as much as 45 days old. So, it's best for funds with a long-term (usually value-oriented) approach. As one example, here's the latest filing from Seth Klarman's Baupost Group.

And in case you're interested, here's one for Bernard L. Madoff Investment Securities LLC (I hear the founder has been in the news lately).

HT: World Beta who uses this information in an investment screening tool.

Wednesday, December 17, 2008

When Worlds Collide: Spitzer Lost Money With Madoff

From Clusterstock.com: Elliott Spitzer Lost Money With Madoff:

I love it when two stories intersect (however loosely). It sounds like the Seinfeld episode "The Pool Guy"when George's girlfriend Susan starts being friends with Elaine.

HT: FinanceProfessor.com

Add the name Eliot Spitzer to the list of prominent people allegedly ripped off by Wall Street trader Bernard L. Madoff. Yesterday at Slate's holiday party Spitzer, who is writing a column for the online publication, confirmed that his family's firm had investments with a Madoff subsidiary.

HT: FinanceProfessor.com

The 12 Days of Global Warming

Whether you believe in global warming or not, this is pretty funny. At least I thought so. And besides--anything that makes fun of Al Gore is always worth a look just on general principles.

Note: If you want to receive updates, either sign up for email on the right sidebar, or add our RSS feed to your feed reader.

Note: If you want to receive updates, either sign up for email on the right sidebar, or add our RSS feed to your feed reader.

Tuesday, December 16, 2008

It's All Done But The Grading (And The Bargaining)

I gave my last exam (to my MBA class) last night. I thought it was a pretty easy one, but as usual, there were three students (out of twenty eight) still working at the end of three hours' time. I've come to the realization that I could give four hours (or even five) for an exam, and there would STILL be a few people working to the bitter end. A few observations from the exam (none of them surprising):

Oh wait - I already got one of those...

- My favorite student got the Terry Pratchett/Discworld references sprinkled on the exam, and one of my others caught a couple of 1980s movie references.

- In between walking up and down the aisles, I wrote about a hundred lines of SAS code

- One of my students already has sent an email asking if we can meet "to discuss his grade." Anyone want to guess how that'll play out?

Oh wait - I already got one of those...

Monday, December 15, 2008

Winner's (and Loser's) Curse with Swoopo.com

Winner's curse is the well-known phenomenon where the winner of an auction is often just the person who's most likely to have overpaid for the item in question. So, often the winner is the loser.

Then I heard about Swoopo.com. It's been called "pure distilled evil in a business plan". Here's their setup:

They also hold "penny auctions" on their front page - a bid only increments the price by a penny. I recently saw a TomTom GPS sold for about $12. That means 1200 bids at $0.75 per bid, for revenue of $900, on something that costs them between $300 and $500. Not too shabby.

This is a behavioral economist's dream - it has bidders focusing on sunk costs (I have to make back my bids, and if I win, I get the savings), hubris, and endowment effects (the bidders start viewing the item as "theirs", and therefore value it more highly). And if I thought about it a bit, I could probably come up with other behavioral biases.

It has some similarities to a "dollar auction". In this setting, individuals bid on a dollar. But the catch is that the second highest bidder must also pay their bid, but without getting the dollar in exchange. So, the second place bidder continues to escalate to cut their losses. In Swoopo's setup, the 2nd place bidder isn't obligate to pay, but once they're in the game, they continue bidding to recoup their already-paid bids (that is, if they can get the item at a discount).

It's not a scam per se, because everything is disclosed up front - the rules are clearly stated. But the only advice I can give you about using Swoopo comes from War Games (the 1983 movie starring a very young Matthew Broderick):

UPDATE: Here's a perfect example of how the irrational bidding that can take place - a person "won" an auction for a Sharp 42 inch LCD TV. According to the website, it was "worth up to" $1,199. The "winning" bidder paid $3,360. Assuming that this was a "normal" auction with bid increments of $0.15, this means that Swoopo received total bids of (3,360/0.15) x $0.75 = $16,800 in total bids (including $1,512 from the "winner" alone), in addition to the winning bid of $3,360, for a total of $20,160 -- all for an item worth at most $1200.

UPDATE2: as pointed out by a reader, the auction above was a "fixed price" one where the "winner" got to purchase the item for $119. So, the buyer could have potentially gotten it for a very nice proice. However, they ended up spending over $1500 in bids, plus the $119 winning price, all for a TV that was worth at most $1200. So, the winner endend up overpaying by at least $400, and Swoopo made total revenue of almost $17,000 for the cost of a $1200 TV.

One part of me wishes I'd thought of this - in about a couple of days time I'd have made back all the money my retirement accounts lost this past year. But I'd feel a little bad getting that money from stupid people. Not to say I wouldn;t do it, but I'd feel a little bad.

Then I heard about Swoopo.com. It's been called "pure distilled evil in a business plan". Here's their setup:

- Bidding for an item starts at $0.15

- Each bid raises the price by $0.15

- Bids cost $0.75 to make.

- Here's the kicker - a bid in the final seconds extends the auction for 15 seconds. So, auctions can go on and on.

They also hold "penny auctions" on their front page - a bid only increments the price by a penny. I recently saw a TomTom GPS sold for about $12. That means 1200 bids at $0.75 per bid, for revenue of $900, on something that costs them between $300 and $500. Not too shabby.

This is a behavioral economist's dream - it has bidders focusing on sunk costs (I have to make back my bids, and if I win, I get the savings), hubris, and endowment effects (the bidders start viewing the item as "theirs", and therefore value it more highly). And if I thought about it a bit, I could probably come up with other behavioral biases.

It has some similarities to a "dollar auction". In this setting, individuals bid on a dollar. But the catch is that the second highest bidder must also pay their bid, but without getting the dollar in exchange. So, the second place bidder continues to escalate to cut their losses. In Swoopo's setup, the 2nd place bidder isn't obligate to pay, but once they're in the game, they continue bidding to recoup their already-paid bids (that is, if they can get the item at a discount).

It's not a scam per se, because everything is disclosed up front - the rules are clearly stated. But the only advice I can give you about using Swoopo comes from War Games (the 1983 movie starring a very young Matthew Broderick):

UPDATE: Here's a perfect example of how the irrational bidding that can take place - a person "won" an auction for a Sharp 42 inch LCD TV. According to the website, it was "worth up to" $1,199. The "winning" bidder paid $3,360. Assuming that this was a "normal" auction with bid increments of $0.15, this means that Swoopo received total bids of (3,360/0.15) x $0.75 = $16,800 in total bids (including $1,512 from the "winner" alone), in addition to the winning bid of $3,360, for a total of $20,160 -- all for an item worth at most $1200.

UPDATE2: as pointed out by a reader, the auction above was a "fixed price" one where the "winner" got to purchase the item for $119. So, the buyer could have potentially gotten it for a very nice proice. However, they ended up spending over $1500 in bids, plus the $119 winning price, all for a TV that was worth at most $1200. So, the winner endend up overpaying by at least $400, and Swoopo made total revenue of almost $17,000 for the cost of a $1200 TV.

One part of me wishes I'd thought of this - in about a couple of days time I'd have made back all the money my retirement accounts lost this past year. But I'd feel a little bad getting that money from stupid people. Not to say I wouldn;t do it, but I'd feel a little bad.

Some Links On Distressed Debt Investing

One of my students is interviewing soon for an internship in an investment bank's fixed income department, and another is going to be starting soon in a credit analyst position, So, these pieces on distressed debt investing were pretty timely.

Michelle Harner over at the Conglomerate posted a very nice piece with some links about distressed debt investing. She highlights the difference between "vulture investing" and "investing for control" (basically traders vs. longer-term investors). She gives a couple of pretty good references. One, from Knowledge@QWharton lays out the basics of "distressed for control" investing:

She also cites some of her own research: a survey titled "Trends In Distressed Debt Investing: An Empirical Study of Investors' Objectives" (available on SSRN here).

Finally, Marketwatch gives us a look into the world of "vulture investors." It's a bit dated (April), but it shows how busy the world of distressed debt has become. One of the guys at my church's men's group is an analyst at a local distressed-debt hedge fund. He said he hasn't had this many good choices to buy since he can remember (luckily his firm is sitting on some cash).

I'm teaching the Level 1 Fixed Income material for CFA this spring, and will be teaching Unknown University's Fixed Income class in the fall. So, I'll probably be posting more on the credit market topics as time goes on (I tend to use this blog as a handy place to keep class-related stuff I want to remember).

Michelle Harner over at the Conglomerate posted a very nice piece with some links about distressed debt investing. She highlights the difference between "vulture investing" and "investing for control" (basically traders vs. longer-term investors). She gives a couple of pretty good references. One, from Knowledge@QWharton lays out the basics of "distressed for control" investing:

Simply put, their line of work is to make a profit from companies that have failed to do so and are on the brink of bankruptcy. Unlike traditional hedge funds, however, their investment doesn't stop at buying significant portions of these companies' debt for pennies on the dollar, tidying up the balance sheet and then selling at a higher price. Instead, KPS and Matlin Patterson get in and stay in -- bringing in new managers, installing a new strategy, renegotiating labor and supplier contracts, and so on. (That's the 'control' part.) It's not an easy task, especially given the state of these companies when they step in.Read the whole thing here.

She also cites some of her own research: a survey titled "Trends In Distressed Debt Investing: An Empirical Study of Investors' Objectives" (available on SSRN here).

Finally, Marketwatch gives us a look into the world of "vulture investors." It's a bit dated (April), but it shows how busy the world of distressed debt has become. One of the guys at my church's men's group is an analyst at a local distressed-debt hedge fund. He said he hasn't had this many good choices to buy since he can remember (luckily his firm is sitting on some cash).

I'm teaching the Level 1 Fixed Income material for CFA this spring, and will be teaching Unknown University's Fixed Income class in the fall. So, I'll probably be posting more on the credit market topics as time goes on (I tend to use this blog as a handy place to keep class-related stuff I want to remember).

Sunday, December 14, 2008

It's Final Exam Time

I give my last final exam of the semester tomorrow to my MBAs. Just for the heck of it, I named all the companies and individuals in the problems after characters from Terry Pratchett's Discworld novels. I wonder if anyone in the class will notice?

If they do, I'll probably give them extra credit.

If they do, I'll probably give them extra credit.

Bill Miller: The Stock Picker's Defeat

From 1991 to 2005, Bill Miller (superstar mutual fund manager for Legg Mason's Value Trust) beat the S&P every year - a record no other manager has ever come close to matching. Then, this last year the bottom fell out and his fund lost 58% (about 20% more than the typical fund.

The Wall Street Journal has a great interview of Miller, and here's the best line:

The Wall Street Journal has a great interview of Miller, and here's the best line:

This meltdown has provided a lesson for Mr. Miller and other "value" investors: A stock may look tantalizingly cheap, but sometimes that's for good reason.It's a very good piece for discussing in class, since it touches on a lot of issues related to market efficiency. Read the whole thing here.

Saturday, December 13, 2008

When Diversification Doesn't Work

I'm not sure, but I think it has something to do with correlation...

Tuesday, December 09, 2008

The Long-Run and International Evidence on the Value Premium

The term "Value Premium" refers to the empirical observation that firms with low price multiples (i.e Price/Book, Price/Earnings, Price/Cash Flow) have tended to have higher returns than their high-multiple counterparts - even after controlling for risk. People give a lot of possible reasons for this - we have a bad model for controlling for risk, there are behavioral biases, or it's simply a case of data diving.

I just came across a paper by a group known as the Brandeis Institute titled "Value vs. Glamour: A Global Phenomenon" that seems to rule out the data diving story. They examine the evidence for the value premium both across time (the mid 1960's to the present) and internationally. They found that

HT: CXO Advisory Group

I just came across a paper by a group known as the Brandeis Institute titled "Value vs. Glamour: A Global Phenomenon" that seems to rule out the data diving story. They examine the evidence for the value premium both across time (the mid 1960's to the present) and internationally. They found that

While the degree of outperformance of value stocks vs. glamour stocks varied across data sets, what strikes us as most significant was the consistency the value premium exhibited:The paper has a lot of nice graphs that could be useful in class. You can read the whole thing here.

- across valuation metrics, such as price-to-book, price-to-cash flow, price-to-earnings,and sales growth

- across time, which in this study applies to the 1968-2008 period for U.S. stocks,and the 1980-2008 period for non-U.S. stocks

- across regions, as the results indicated a value premium in developed markets in North America, Europe, and Asia

- across market capitalizations, as the relative outperformance of value stocks to glamour stocks was evident among both large- and small-cap stock universes.

HT: CXO Advisory Group

Friday, December 05, 2008

The Final Throes of the Semester

It's that time of the semester:

The crop is almost in. And man, oh man is it about time.

One of the things I like about this career is that it has a rhythm to it - we have new "crops" each semester, and a feeling of accomplishment once the semester is done. But that final week or two is always a bit crazy.

So, to all my readers: If you're a student, good luck on your exams and projects. If you're faculty, hang in there - it's almost time for the break.

- Only one meeting left for each of my classes.

- My student-managed fund survive their end-of semester presentation to the advisory board

- I've graded and handed back all assignments except for final exams

- I've even given out and collected my evaluations

The crop is almost in. And man, oh man is it about time.

One of the things I like about this career is that it has a rhythm to it - we have new "crops" each semester, and a feeling of accomplishment once the semester is done. But that final week or two is always a bit crazy.

So, to all my readers: If you're a student, good luck on your exams and projects. If you're faculty, hang in there - it's almost time for the break.

Wednesday, December 03, 2008

New Blog on Markets

Al Roth (the George Gund Professor of Economics at Harvard) is extremely well known in the fields of game theory and market design. For just a few examples, he's published highly cited work on the market for donor organs, matching medical students with residencies, and matching public school children with schools. He also

Now he has a blog, titled (appropriately enough) Market Design. It's definitely worth a look-see.

HT: Marginal Revolution

Now he has a blog, titled (appropriately enough) Market Design. It's definitely worth a look-see.

HT: Marginal Revolution

Monday, December 01, 2008

Credit Default Swaps and Arctic Expeditions

This weekend I posted a video of a "whiteboard" talk by Paddy Hirsch of Marketplace, in which he explains CDOs and the credit crisis. Here's another one where he explains Credit Default Swaps (CDS) using the analogy of an arctic expedition.

Since I'm teaching Fixed Income next year, I'm sure some of these will make their way into my class.

Since I'm teaching Fixed Income next year, I'm sure some of these will make their way into my class.

Sunday, November 30, 2008

We've Had Some Budget Cuts

Yes, like most state schools, Unknown University had had some budget cuts - about 10% so far from the original budget. So these three strips by Scott Adams were pretty funny. A bit close to home, but funny.

Saturday, November 29, 2008

One of The Best Explanations of the Credit Crisis I've Ever Seen

Every once in a while you come across an explanation that makes you realize that just really aren't all that good a teacher. Here's another one to add to the pile. In this video, Marketplace Senior Editor Paddy Hirsch gives one of the best explanations of CDOs and how they contributed to the current credit market woes that I've yet seen:

He's also got some other videos up on YouTube that I'll post in the next couple of weeks.

He's also got some other videos up on YouTube that I'll post in the next couple of weeks.

Thursday, November 27, 2008

Happy Thanksgiving

Here's wishing a Happy Thanksgiving to you and yours from the Unknown Family. We've got a great, great many things to be thankful for - job, family, health, living situation, etc...). For now, we're off to the Unknown Sister-in-Law's house to engage in some extreme eating - three sisters in the family, and all (and Grandma, too) are great cooks.

Now go overdose on Tryptophan.

Now go overdose on Tryptophan.

Wednesday, November 26, 2008

(Bad) Governance at The University

For good corporate governance, it's important that the independent directors on the board are really independent. In particular, they shouldn't have business relationships with the company other their board service. If they did, it would make it hard for them to rein in the CEO, for fear that they'd lose the business.

There's been tons of work on this topic both in the academic and practitioner literatures. But I haven't seen much on similar relationships for universities. I'm sure that a lot's been done- I just haven't seen it.

Until now.

There's a good illustration in the Boston Globe of directors at Suffolk University (actually, trustees, which serve a similar role for a university) with significant business ties to the school. It turns out they just awarded the University president a 2.8 million dollar pay package. Of course, there were "good reasons" for doing so. Here's the lede from the story:

As an aside, if you want to see some excellent examples of affiliated directors in the corporate world (along with other examples of bad governance), there's no better place to go than Michelle Lederer's Footnoted.org. She's made a career out of scouring through company documents to find some truly outrageous examples of corporate mis-governance.

I think the president of Unknown University considered having some trustees with business ties to the school, but we didn't have enough money to pay the required graft.

There's been tons of work on this topic both in the academic and practitioner literatures. But I haven't seen much on similar relationships for universities. I'm sure that a lot's been done- I just haven't seen it.

Until now.

There's a good illustration in the Boston Globe of directors at Suffolk University (actually, trustees, which serve a similar role for a university) with significant business ties to the school. It turns out they just awarded the University president a 2.8 million dollar pay package. Of course, there were "good reasons" for doing so. Here's the lede from the story:

Boston lobbyist Robert Crowe was key among the Suffolk University trustees who made David J. Sargent the highest paid university president in the nation in 2006, with a $2.8 million compensation package. Less than a year later, Sargent renewed a $10,000-a-month contract with Crowe's lobbying firm to represent Suffolk's interests in Washington.

This month, as controversy flares over Sargent's pay, the job of publicly defending it falls on George Regan, himself a new appointee to the Suffolk Board of Trustees as well as the beneficiary of a $366,000 annual contract with the university.

Read the whole thing here.

Is this necessarily a bad thing? Not really - it could be perfectly innocent, and it's not surprising that trustees of a university might have significant business ties to the university. After all, they tend to be prominent alumni with a long history with the school. But, when you have those ties, a pay package like that is going to get far greater scrutiny than it would otherwise. Or as Ricky Ricardo would have said, "they got some 'splainin to do".As an aside, if you want to see some excellent examples of affiliated directors in the corporate world (along with other examples of bad governance), there's no better place to go than Michelle Lederer's Footnoted.org. She's made a career out of scouring through company documents to find some truly outrageous examples of corporate mis-governance.

I think the president of Unknown University considered having some trustees with business ties to the school, but we didn't have enough money to pay the required graft.

Monday, November 24, 2008

All The Monty Python You Could Ever Want

At this point in the semester, we're all tired, frustrated, and looking towards the end of the term. So things that make us laugh become even more important. Luckily, there's now a Monty Python YouTube Channel. Here's the announcement from the MP boys themselves:

HT: Barry Ritholtz.

For the lawyers, here's the disclaimer:For 3 years you YouTubers have been ripping us off, taking tens of thousands of our videos and putting them on YouTube. Now the tables are turned. It's time for us to take matters into our own hands.

We know who you are, we know where you live and we could come after you in ways too horrible to tell. But being the extraordinarily nice chaps we are, we've figured a better way to get our own back: We've launched our own Monty Python channel on YouTube.

No more of those crap quality videos you've been posting. We're giving you the real thing - HQ videos delivered straight from our vault.

What's more, we're taking our most viewed clips and uploading brand new HQ versions. And what's even more, we're letting you see absolutely everything for free. So there!

But we want something in return.

None of your driveling, mindless comments. Instead, we want you to click on the links, buy our movies & TV shows and soften our pain and disgust at being ripped off all these years.

Website: http://pythonline.com

Warning- clicking on the link can result in hours of time wasted, a skewed perspective on life, and adoption of British accents.Now go and enjoy.

HT: Barry Ritholtz.

Friday, November 21, 2008

The NYU Finance Department Has a Blog!

NYU has one of the largest and best finance faculties around (most surveys place them squarely in the top 5 programs in terms of research output). It turns out that they now have a blog: Stern Finance.

It looks pretty promising. Although it's less than 2 months old (the first post was made on September 26), it already has a lot of high-quality content, with participation from a pretty large nuimnber of the faculty. Just this last month, it has posts by Viral Acharya, Marti Subramanyam, Edward Altman, and Joel Hasbrouk among others).

It's definitely one to add to your feed reader.

It looks pretty promising. Although it's less than 2 months old (the first post was made on September 26), it already has a lot of high-quality content, with participation from a pretty large nuimnber of the faculty. Just this last month, it has posts by Viral Acharya, Marti Subramanyam, Edward Altman, and Joel Hasbrouk among others).

It's definitely one to add to your feed reader.

Thursday, November 20, 2008

Tuesday, November 18, 2008

Mark Cuban Charged With Insider Trading By SEC

Mark Cuban, HDnet founder and owner of the Dallas Mavericks was just charged with insider trading by the SEC. The commission alleges that Cuban received a call from tje Mamma.com CEO about a pending PIPE offering of Mamma's stock. The call was supposedly prefaced by a disclaimer from the CEO that the information was confidential. The SEC complaint alleges that Cuban then used this insider information to sell all his Mamma.com shares in after-hours trading, thereby avoiding a loss of about $750,000. In case you're interested, here's a link to the complaint.

It should make for an interesting case. Cuban has the resources to fight this thing pretty much as far as he wants (even potentially all the way to the Supreme Court), and is definitely stubborn enough to do exactly that. He's already posted a response to the complaint on his blog:

In the meanwhile, I have SAS programs to run and papers to write.

It should make for an interesting case. Cuban has the resources to fight this thing pretty much as far as he wants (even potentially all the way to the Supreme Court), and is definitely stubborn enough to do exactly that. He's already posted a response to the complaint on his blog:

Mr. Cuban stated, “I am disappointed that the Commission chose to bring this case based upon its Enforcement staff’s win-at-any-cost ambitions. The staff’s process was result-oriented, facts be damned. The government’s claims are false and they will be proven to be so.”Not surprisingly, Stephen Bainbridge has a very thorough legal analysis of the issue. After all, it's in his wheelhouse.

In the meanwhile, I have SAS programs to run and papers to write.

Thursday, November 13, 2008

Weird Happenings on My Feeds

In the last few days, I've noticed big fluctuations in my feed readership along with a lot of strange things on Bloglines: all of a sudden, 200 new posts are listed for one blog or another. Is this happening to everyone, or just to me because of the last few political cartoons I posted?

Wednesday, November 12, 2008

A Churchill Quote Relevent to the Current Economic Crisis

Compliments of Newmark's Door

In fact, my favorite Churchill story is the one about the time that Churchill was standing at the urinal in the men's room of the House of Commons. Atlee came into the room and stood at the urinal next to Winston's. Churchill looked up at him, zipped up, moved a couple of urinals farther down and resumed his business. "Why Winston, I had no idea you were so modest.", said Atlee. "It's not modesty, Prime Minister. It's only that every time you find something that is large and functions well, you try to nationalize it, and I thought it best not to take a chance!".What will they nationalize next?

The Financial Crisis From A To Z

Tunku Varadarajan at Forbes has a pretty clever piece titled "The Financial Crisis From A-Z". Here are a few of the items that tickled my fancy:

HT: The Big Picture.

C is for Credit Default Swaps, defined for me by a Wall Street watcher as: Risk whatever you want, and we insure it; risk too much, taxpayers insure it.The other 21 letters are pretty good too. Read the whole thing here.

L is for leverage (a means of maximizing your losses), liar loans, Lehman (pronounced "lemon")--and the losses/liabilities that unite them all.

M is for where it all started: the mortgage (which, aptly, means death-pledge). Like the dog, it comes in a variety of breeds, "sub-prime" being a cross between a pit bull and a chihuahua.

Q is for quants, who forgot that, every so often, past performance is no indicator of anything at all.

S is for securitization, the process by which one passes off cat food as caviar.

HT: The Big Picture.

Monday, November 10, 2008

New Blog

As a new blogger, Financial Rounds benefitted from a number of higher-profile bloggers mentioning it. So, I think it's important to pay the favor forward and highlight new blogs of note.

The latest new one is a put out by The Applied Portfolio Management Program at Washburn University.

Unlike other academic blogs, this one is unique in that material is contributed both by faculty and by students in the program.

Go check it out, and add them to your feed reader - it's been added to the blogroll. And if you come across any other ones, drop me a line.

The latest new one is a put out by The Applied Portfolio Management Program at Washburn University.

Unlike other academic blogs, this one is unique in that material is contributed both by faculty and by students in the program.

Go check it out, and add them to your feed reader - it's been added to the blogroll. And if you come across any other ones, drop me a line.

Friday, November 07, 2008

Professor Time vs. Grad Student Time

That reminds me - I have to check up on my grad assistant to see how he's doing on the assignment I gave him at the beginning of the semester.

Great Source For Financial Information

The student-managed investment fund class I teach is fortunate to be in a trading room with a lot of resources - because of a prominent alumni, we have access to everything from analyst reports to trade and quote data. But for those who don't have these resources, check out Tickerpedia - it has analyst forecasts, recommendations, SEC filings, a neat chart of ratios from various sources, and much more.

It's interesting how much the reported ratios change by data source. As one example, for GATX corp, the reported operating margin (trailing 12 months) ranged from 18.92% (reported on Reuters) to 46.7% (on Marketwatch).

HT: Jim Mahar at Finance Professor

It's interesting how much the reported ratios change by data source. As one example, for GATX corp, the reported operating margin (trailing 12 months) ranged from 18.92% (reported on Reuters) to 46.7% (on Marketwatch).

HT: Jim Mahar at Finance Professor

Thursday, November 06, 2008

Post Election Analysis From South Park

Compliments of South Park. Hey - I suspected it was an insidious plot of some kind all along.

Caution - may not be safe for work, unless you can close your office door and turn the audio WAY down.

Caution - may not be safe for work, unless you can close your office door and turn the audio WAY down.

Wednesday, November 05, 2008

A Joke For The Science Nerds

Apropos of nothing:

Update: if you haven't managed to get your geek on, click here (hey - a couple of people asked, and I'm nothing if not accommodating).

Don't ask me why - I just thought it was funny.

Heisenberg gets pulled over by the cops for speeding. Cop walks up to his care and asks,"sir, do you have any idea how fast you were going?"

Heisenberg replies, "no, but I know exactly where I am."

Update: if you haven't managed to get your geek on, click here (hey - a couple of people asked, and I'm nothing if not accommodating).

Can I Bwing My Mommy? Puh-Weeze?

A new student (I'll call him SnowFlake from now on) walked into my office last week asking for advice on classes. He'd transferred to Unknown University from a private school (which, by the way, has a reputation for drastically inflating grades). He needed some advice on which classes to take, and since I'm listed as his advisor, I seemed like the right person to check with. But he also wanted some advice on how to study since he's flunking intermediate accounting, and "that's never happened in any of my classes before".

SnowFlake starts out by blaming the instructor (who, by the way, is one of the best in the college). After some questions and comments on my part like "Gee, that doesn't sound like Professor X at all. Are you sure?", it turns out that he hadn't been keeping up with the work, and hadn't worked more than a problem or two from the end of chapter material. Instead, he tried to cram for the first exam, and did poorly. Since that strategy worked out so well on the first exam, he decided to try it once more on the second exam for good measure. Lo and behold, the same approach yielded the same result (funny how that happens).

So, I gave Snowflake some standard advice on how to study, and then he asked if he could set up a time early this week to set up his classes for the next semester. We set a time (Monday morning at 10), and then came the kicker:

He asked if it was alright if his MOTHER came to the appointment.

I managed to keep my jaw off the floor, since he was a second-semester junior, and if you have hover-moms, they usually get cured of it by sophomore year (and they're almost non-existent in Business schools). But since I couldn't think of anything else to say (other than "You'll be all right once they drop", which didn't seem prudent at this juncture). I said, "Well, Precious, that's entirely up to you".

Monday morning comes around, and I'm running late for our 10:00 a.m. appointment. So, I have the secretary leave a note on my door saying I'd be a few minutes late, and hurry in to the office with visions of MomZilla running loose in the hallway and going on a rampage in the Dean's office.

I get there five minutes late, and there's no sign of either Snowflake or MomZilla. I hang out in my office for a few hours just in case, and it seems like a larger-than-usual number of faculty seem to filter by my office (they keep me off the beaten path, which is probably a good thing). I guess after hearing about Mom coming in, they just couldn't resist sneaking a peek.

In any event, I get a call late that morning from SnowFlake informing me that he had to be in traffic court that morning, had completely forgotten, and wanted to reschedule.

I guess I should have had his Mom remind him.

SnowFlake starts out by blaming the instructor (who, by the way, is one of the best in the college). After some questions and comments on my part like "Gee, that doesn't sound like Professor X at all. Are you sure?", it turns out that he hadn't been keeping up with the work, and hadn't worked more than a problem or two from the end of chapter material. Instead, he tried to cram for the first exam, and did poorly. Since that strategy worked out so well on the first exam, he decided to try it once more on the second exam for good measure. Lo and behold, the same approach yielded the same result (funny how that happens).

So, I gave Snowflake some standard advice on how to study, and then he asked if he could set up a time early this week to set up his classes for the next semester. We set a time (Monday morning at 10), and then came the kicker:

He asked if it was alright if his MOTHER came to the appointment.

I managed to keep my jaw off the floor, since he was a second-semester junior, and if you have hover-moms, they usually get cured of it by sophomore year (and they're almost non-existent in Business schools). But since I couldn't think of anything else to say (other than "You'll be all right once they drop", which didn't seem prudent at this juncture). I said, "Well, Precious, that's entirely up to you".

Monday morning comes around, and I'm running late for our 10:00 a.m. appointment. So, I have the secretary leave a note on my door saying I'd be a few minutes late, and hurry in to the office with visions of MomZilla running loose in the hallway and going on a rampage in the Dean's office.

I get there five minutes late, and there's no sign of either Snowflake or MomZilla. I hang out in my office for a few hours just in case, and it seems like a larger-than-usual number of faculty seem to filter by my office (they keep me off the beaten path, which is probably a good thing). I guess after hearing about Mom coming in, they just couldn't resist sneaking a peek.

In any event, I get a call late that morning from SnowFlake informing me that he had to be in traffic court that morning, had completely forgotten, and wanted to reschedule.

I guess I should have had his Mom remind him.

Tuesday, November 04, 2008

We Voted

The Unknown Family just went to the polls and voted. Unknown Son went into the booth with me, and Unknown Daughter went in with the Unknown Wife. We let our kids fill out the ballots (they were paper ones), and then feed them into the machine.

It's pretty cool explaining how our political system works to an 8 year old and a ten year old. This year, I think I'll start working through the Declaration of Independence, the Constitution, and the Bill of Rights with them - it's never too early, and most people (myself included) don't know enough about these foundations of our country.

It's pretty cool explaining how our political system works to an 8 year old and a ten year old. This year, I think I'll start working through the Declaration of Independence, the Constitution, and the Bill of Rights with them - it's never too early, and most people (myself included) don't know enough about these foundations of our country.

Friday, October 31, 2008

Happy Halloween

I usually don't post political stuff (because of the moonbat factor). But I just got this from a former student and it tickled me, so what the heck.

Tuesday, October 28, 2008

Godspeed, Dean Barnett

I've always enjoyed Dan Barnett's writing and commentary, whether at SoxBlog, the Weekly Standard, or guesting on Hugh Hewitt's radio show. I just heard that he passed away after a long fight against Cystic Fibrosis. He was clearly one of the good guys. To get a small sense of the man, read this excerpt from his pamphlet "The Plucky Smart Kid With The Fatal Disease: A Life With Cystic Fibrosis"

To see a list of tributes to the man at the Weekly Standard, click here.

As I grew sicker, I had what for me was an extremely comforting insight. I came to view serious and progressive illness as an ever constricting circle with oneself at the center. The interior of the circle represents the contents of one’s life. As the circle gets smaller, things that were inside get forced out. Some of these things are dearly missed; others that were once thought precious get forced to the exterior and turn out to go surprisingly unlamented.

t the innermost point of the circle are the things that really matter: family, faith, love. These things stay with you until the day you die. At the very end, because the circle has shrunk down to its center, they’re all you have left. But as we approach that end, we finally realize that all along, they were what mattered most. As a consequence, life often remains beautiful and worthwhile right up until the end.A quick reminder: we're all born with a fatal ailment - it's called life, and no one gets out alive at the end. So without getting overly schmaltzy or preachy, we'd all do well to spend more time on that "inner circle" than Barnett wrote about.

To see a list of tributes to the man at the Weekly Standard, click here.

Monday, October 27, 2008

Finance and Economic Courses on the Web on The Web

Increasingly, people are putting their lectures, teaching material, and (in some cases), entire courses on the web. Here are a few I've recently come across:

A Short Course In Behavioral Economics: Daniel Kahneman (yes, the Nobel Laureate) has recorded and posted videos of a two day conference called "Thinking about Thinking".

Robert Schiller's Spring 2008 Financial Markets Class at Yale: Schiller has done a great deal of work in market efficiency, and also created the Case-Schiller Index of Home Prices.

While surfing through Yale's Open Classes, I also found a class titled Game Theory, by Ben Polak, a widely published economist. He seems to cover all the big topics: Nash (and other) Equilibrium concepts, Adverse Selection, Signalling, and even Evolutionary Game Theory.

If you know of other finance/econ classes on the web, let me know in the comments section and I'll post them here.

A Short Course In Behavioral Economics: Daniel Kahneman (yes, the Nobel Laureate) has recorded and posted videos of a two day conference called "Thinking about Thinking".

Robert Schiller's Spring 2008 Financial Markets Class at Yale: Schiller has done a great deal of work in market efficiency, and also created the Case-Schiller Index of Home Prices.

While surfing through Yale's Open Classes, I also found a class titled Game Theory, by Ben Polak, a widely published economist. He seems to cover all the big topics: Nash (and other) Equilibrium concepts, Adverse Selection, Signalling, and even Evolutionary Game Theory.

If you know of other finance/econ classes on the web, let me know in the comments section and I'll post them here.

Wednesday, October 22, 2008

You Get What You Pay For: Designing Incentive Compensation Plans

While I'm not currently working in that area, I try to keep on on topics related to compensation design and effects. One of the ongoing themes of this literature is that a program designed to incent employees to do one thing often has unintended consequences. As an example, the Unknown Wife put me through grad school working for a cell phone company. At one point, she was a commission auditor - the job was important because salespeople often tried to make their quotas by miscoding things rather than by just selling more (I'm shocked! Shocked, I say!). So, they needed people like her to check everyone's sales.

There's a great piece on this topic by Joel Sposky in Inc magazine.. Here's a choice snippet:

He's got some great examples illustrating this point. Read the whole thing here.

HT: Craig Newmark

There's a great piece on this topic by Joel Sposky in Inc magazine.. Here's a choice snippet:

I'm always on the lookout for these incentive schemes gone wrong. There's a great book on the subject by Harvard Business School professor Robert Austin -- Measuring and Managing Performance in Organizations. The book's central thesis is fairly simple: When you try to measure people's performance, you have to take into account how they are going to react. Inevitably, people will figure out how to get the number you want at the expense of what you are not measuring, including things you can't measure, such as morale and customer goodwill.

...His point is that incentive plans based on measuring performance always backfire. Not sometimes. Always. What you measure is inevitably a proxy for the outcome you want, and even though you may think that all you have to do is tweak the incentives to boost sales, you can't. It's not going to work. Because people have brains and are endlessly creative when it comes to improving their personal well-being at everyone else's expense.

HT: Craig Newmark

Monday, October 20, 2008

Are Hedge Funds Good at Reading The Market>

The tentative answer seems to be "Yes".

According to a new study "Unbundling Hedge Fund Betas" by by Ulloa, Giamouridis, Mesomeris, and Noorizadesh there's evidence that hedge funds increase betas prior to market upswings. Here's the abstract:

Read the whole thing (downloadable copy at SSRN) here.

HT: All About Alpha

According to a new study "Unbundling Hedge Fund Betas" by by Ulloa, Giamouridis, Mesomeris, and Noorizadesh there's evidence that hedge funds increase betas prior to market upswings. Here's the abstract:

This article is concerned with the systematic exposures of equity hedge fund managers. In particular we seek common equity hedge fund systematic exposures through rigorous model selection techniques. We study their time variance to examine if equity hedge fund style characteristics are stable through time. Most importantly, we explore the informational role of manager decisions to shift their exposures to certain styles. Our results suggest that equity fund managers are exposed to three dominant style strategies, namely the 'market', 'value' and 'momentum'. We also discover that there is a considerable degree of variability in the factor exposures over time for the various dominant sources of systematic risk/return. Finally, we show evidence that managers vary their exposures to the 'market' in time to exploit favourable market moves. A similar pattern is however not observed for their 'value' or 'momentum' exposures.

HT: All About Alpha

A Hectic Couple of Weeks

It's been a crazy couple of weeks. Some good, some bad. But crazy, nonetheless.

About two weeks ago, I went to the FMA annual meeting in Dallas (it was great, by the way). I managed to connect with a lot of old friends, and also made a few new ones.

While I was there, I started a couple of new projects. Without going into too much detail, I think I've figured out a very creative way to use a data set in a new way. Just before FMA, I started a paper with a couple of grad school classmates that uses this data. While doing it, I realized a slew of different applications for the data and methodology.

In short, it's data that's typically used by researchers in one sub-field of finance, but I think it can be used to answer a number of corporate finance research questions. The data's pretty ugly, so it took a while to get it under control. But now that I've got a handle on it, I have more ideas to use it for than I have time to implement. So, I was looking for coauthors who could help out. Luckily, I have a lot of friends, so there were people willing to listen to the idea(s). As a result, I now have three new projects. They may be garbage and I might be totally deluded that this is a good idea, but I don't think so (or at least, I hope not).

Once I got back, I bought a "new" (to me) used car, taught in our evening MBA program one night and then twice in a neighboring city in a professional program, and had two family health problems.

Unknown Son had his surgical port removed (now that he's done with chemo, he no longer needs it, and it is a risk for infection). Unfortunately, what should have been a fairly straightforward half-day affair ended up with him staying overnight at the hospital due to some complications (he's fine now, by the way). Then, the next day Unknown Daughter came down with an intestinal bug that resulted in output from both ends.

Ah well - parenthood involves a lot of bodily fluids, I guess.

In any event, I'm now giving an exam to my evening MBA class. Hey - I have to kill the 2 1/2 hours sometime, eh?

About two weeks ago, I went to the FMA annual meeting in Dallas (it was great, by the way). I managed to connect with a lot of old friends, and also made a few new ones.

While I was there, I started a couple of new projects. Without going into too much detail, I think I've figured out a very creative way to use a data set in a new way. Just before FMA, I started a paper with a couple of grad school classmates that uses this data. While doing it, I realized a slew of different applications for the data and methodology.

In short, it's data that's typically used by researchers in one sub-field of finance, but I think it can be used to answer a number of corporate finance research questions. The data's pretty ugly, so it took a while to get it under control. But now that I've got a handle on it, I have more ideas to use it for than I have time to implement. So, I was looking for coauthors who could help out. Luckily, I have a lot of friends, so there were people willing to listen to the idea(s). As a result, I now have three new projects. They may be garbage and I might be totally deluded that this is a good idea, but I don't think so (or at least, I hope not).

Once I got back, I bought a "new" (to me) used car, taught in our evening MBA program one night and then twice in a neighboring city in a professional program, and had two family health problems.

Unknown Son had his surgical port removed (now that he's done with chemo, he no longer needs it, and it is a risk for infection). Unfortunately, what should have been a fairly straightforward half-day affair ended up with him staying overnight at the hospital due to some complications (he's fine now, by the way). Then, the next day Unknown Daughter came down with an intestinal bug that resulted in output from both ends.

Ah well - parenthood involves a lot of bodily fluids, I guess.

In any event, I'm now giving an exam to my evening MBA class. Hey - I have to kill the 2 1/2 hours sometime, eh?

Wednesday, October 08, 2008

Snl Bailout Skit

Here's a great spoof piece from Saturday Night Live. No one escapes getting tweaked here - Pelosi, Frank, Soros, Flippers, Liars (sometimes they're the same people), or Bush.

SNP subsequently pulled the piece, but someone saved a copy here.

SNP subsequently pulled the piece, but someone saved a copy here.

Wednesday, October 01, 2008

Fear Hits CD Market

I just heard an interesting story from a colleague (a former Wall Street lawyer who decided to become a lecturer at my university after retiring from his former career). I'm sure I'll be using it in class as an example of overreaction for the next few years (hey - I still talk about the Carter Years.

My colleague opened up his brokerage statement and noticed something verrrrry interesting (as Arte Johnson would have said).

He had two negotiable CDs - one from Washington Mutual and one from Lehman Bank. They originally had a 5-year maturity, but now had roughly 6 months until expiration, and were both under the FDIC limit. Here's the kicker - they were quoted at 92 and 93. In other words, you could buy them at 92% of face value, and would receive the full face amount at maturity 6 months later. This works out to a compound annual return of over 18% for the one quoted at 92, and about 15 1/2% for the one at 93. And this is for an FDIC-insured instrument.

So, he called his broker to see if there was an error. He was told that a significant number of people panicked when they saw the WAMU or Lehman name, and wanted to get out of their CDs at all costs. So, although the brokerage firm didn't advertise the fact, if my friend wanted to buy more CDs, he could have them at that price.

It's quite a story, and it illustrates how many people overreact in times of stress. 18% in a federally-insured instrument.

Simply amazing.

My colleague opened up his brokerage statement and noticed something verrrrry interesting (as Arte Johnson would have said).

He had two negotiable CDs - one from Washington Mutual and one from Lehman Bank. They originally had a 5-year maturity, but now had roughly 6 months until expiration, and were both under the FDIC limit. Here's the kicker - they were quoted at 92 and 93. In other words, you could buy them at 92% of face value, and would receive the full face amount at maturity 6 months later. This works out to a compound annual return of over 18% for the one quoted at 92, and about 15 1/2% for the one at 93. And this is for an FDIC-insured instrument.

So, he called his broker to see if there was an error. He was told that a significant number of people panicked when they saw the WAMU or Lehman name, and wanted to get out of their CDs at all costs. So, although the brokerage firm didn't advertise the fact, if my friend wanted to buy more CDs, he could have them at that price.

It's quite a story, and it illustrates how many people overreact in times of stress. 18% in a federally-insured instrument.

Simply amazing.

Tuesday, September 30, 2008

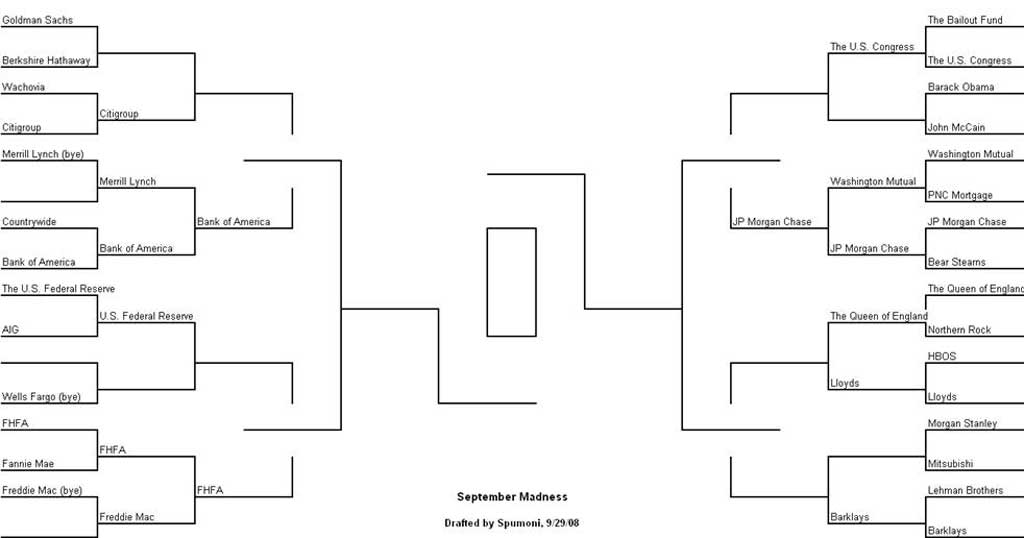

There Shall Be Only One (Bank, that is)

It's too early for March Madness, but here's a pool you can play if you're in the financial services industry - September Madness (click here for a larger version):

HT: Barry Ritholtx

{kind=link}

HT: Barry Ritholtx

A Guide To The Economic Meltdown For Grad Students

If you're a graduate student and worried about how the recent economic turbulence effects you, fear not. The good folks at PhdComics.com have put together a handy guide (click on the picture for a larger version).

Sunday, September 28, 2008

New $700 Billion Hedge Fund

Just to show that not everything in the financial markets is doom and gloom, it turns out that a very large new hedge fund just opened its doors.

HT: one of my readers.

HT: one of my readers.

Wednesday, September 24, 2008

Buffett Buys A Piece of Goldman

It's a good time to be teaching Corporate Finance. Buffett's latest move (making a substantial investment in Goldman Sachs) is bound to make it into a lot of class discussions. The Wall Street Journal's take (at least, as expressed by Georgetown finance professor James Angel) is

Once again, Buffett has been able to make an investment at a very attractive price. In times where there's a lot of turmoil, having cash on hand makes it easy to buy companies (or parts of them) at a bargain, and according to Berkshire's first quarter, they had $31 Billion on hand. So, Buffett had cash at a time when Goldman desperately needed it. As a result, he got a great deal.

Just Damn. That guy is smart.

Berkshire's plan "is a sign of confidence from one of the nation's most respected investors," said James Angel, a finance professor at Georgetown University, who added that "sharp investors" now are "sniffing around the wreckage of the credit crunch to pick up good assets on the cheap."I think the second part of the statement is closer to the truth than the first. Here's what the Sage of Omaha gets for his money

The deal is structured in two parts, giving Berkshire a stream of cash and potential ownership of roughly 10% of Goldman. Berkshire will spend $5 billion on "perpetual" preferred shares of Goldman. These are not convertible into equity but pay a fat 10% dividend.So, while the preferred isn't convertible, he gets what is essentially "synthetic convertible preferred". In essence, he gets his preferred payouts if the stock price doesn't rise, and the option to buy stock at a discount if the price is above $115. So, in effect he has a combination of preferred stock and an in-the-money call option. Barry Ritholtz prices the warrants at approximately $1.5 Billion, giving Buffett an effective yield of 14%, and cites another source who estimates their worth at $3.5B, and a yield of 17%.

Berkshire also will get warrants granting it the right to buy $5 billion of Goldman common stock at $115 a share, which is 8% below the 4 p.m. closing share price Tuesday of $125.05. At Goldman's roughly $50 billion market value, based on that closing price, exercising those warrants would give Berkshire about a 10% stake in Goldman.

Once again, Buffett has been able to make an investment at a very attractive price. In times where there's a lot of turmoil, having cash on hand makes it easy to buy companies (or parts of them) at a bargain, and according to Berkshire's first quarter, they had $31 Billion on hand. So, Buffett had cash at a time when Goldman desperately needed it. As a result, he got a great deal.

Just Damn. That guy is smart.

Tuesday, September 23, 2008

Flaming Wheelchairs

This has nothing to do with finance. Absolutely nothing.

But it caught my eye, and I thought making a blog post with that title would be kind of fun. In addition (as Dave Barry would say), it would make a good name for a rock bank.

Enough bloggery. Time to torture some data.

But it caught my eye, and I thought making a blog post with that title would be kind of fun. In addition (as Dave Barry would say), it would make a good name for a rock bank.

Enough bloggery. Time to torture some data.

Another Crazy Couple of Days

It's been a busy few days. On Saturday, Unknown Son and I took part in his Cub Scout troop's annual popcorn sale outside a local supermarket.

I gave him a little coaching on the way over (i.e. make sure you ask everyone that comes out, look them in the eye, don;t take the first "no" without asking again, and so on). The kid absolutely hung the moon. He sold about 50% more than the other two kids that were there, and the grownups standing around really got a kick out of watching him. It's hard to say no to a determined, charming, and extremely cute 9-year old (of course, I'm completely unbiased).

Sunday was mostly used for prepping for my week's classes (I teach MBAs on Monday evenings, and other classes on Tuesdays and Thursdays). Unfortunately, U.S. started getting a fever Sunday night. We took him into the oncology clinic Monday morning (he had a regular appointment set up anyway), and they sent us home, feeling that it was likely a virus of some kind (no evidence of anything on his scans, and no signs of a bacterial infection). But, by the time I got out of class at 9:00, his fever was spiking to 103.

The doctor didn't seem to feel like he needed to come back in (it's about a 30 mile drive), so we gave him Tylenol, Motrin, and a cool bath, and his fever eventually broke around 1:00 in the morning.

So, I guess I start the week sleep deprived. What else is new.

ed: I had previously written that Unknown Son was 19. That's only in his ability to argue. Chronologically, he's only 9.

I gave him a little coaching on the way over (i.e. make sure you ask everyone that comes out, look them in the eye, don;t take the first "no" without asking again, and so on). The kid absolutely hung the moon. He sold about 50% more than the other two kids that were there, and the grownups standing around really got a kick out of watching him. It's hard to say no to a determined, charming, and extremely cute 9-year old (of course, I'm completely unbiased).

Sunday was mostly used for prepping for my week's classes (I teach MBAs on Monday evenings, and other classes on Tuesdays and Thursdays). Unfortunately, U.S. started getting a fever Sunday night. We took him into the oncology clinic Monday morning (he had a regular appointment set up anyway), and they sent us home, feeling that it was likely a virus of some kind (no evidence of anything on his scans, and no signs of a bacterial infection). But, by the time I got out of class at 9:00, his fever was spiking to 103.

The doctor didn't seem to feel like he needed to come back in (it's about a 30 mile drive), so we gave him Tylenol, Motrin, and a cool bath, and his fever eventually broke around 1:00 in the morning.

So, I guess I start the week sleep deprived. What else is new.

ed: I had previously written that Unknown Son was 19. That's only in his ability to argue. Chronologically, he's only 9.

Wednesday, September 17, 2008

Another Paper Done

I spent most of the last week working on a paper for a conference deadline on Monday. We managed to get the thing done Sunday night (I was in my office until 1:00 a.m. Sunday morning), and planned on submitting it Monday after one last quick read-through. Of course, on Monday morning we got an email announcing that the deadline had been extended. We should have expected it since this happens almost every year for this conference (the Eastern Finance Association annual meeting).

So, we gave the paper one last thorough going over. It was sent out today. It' s early, and the paper will need a lot more work (and polishing) before it's ready to submit to a journal. But the initial results look good, and it's always satisfying to have a finished version (even if it's preliminary) of a paper.

I like working with these coauthors. It's the first time I've worked simultaneously with two fellow alumni of the Unknown Alma Mater, and the initial experience has been very, very good.

So, we gave the paper one last thorough going over. It was sent out today. It' s early, and the paper will need a lot more work (and polishing) before it's ready to submit to a journal. But the initial results look good, and it's always satisfying to have a finished version (even if it's preliminary) of a paper.

I like working with these coauthors. It's the first time I've worked simultaneously with two fellow alumni of the Unknown Alma Mater, and the initial experience has been very, very good.

McCain and Obama Presidential Futures Contracts

I talk about the Intrade Political Futures markets a lot in my classes. They're a good example of how markets process dispersed information. There's a lot of debate about whether they actually predict many kinds of events or merely (in the case of the Presidential elections) merely react to polls. But despite that, they're a fairly simple market that's useful for demonstrating a number of concepts about markets (expected values, bud-ask spreads, trading volume, etc...).

Also, I'm a political junkie, so it's fun to see students in a finance class actually think about politics in a different way.

In any event, it now seems like the McCain for President contract and the Obama contracts have switched places (they're trading at $0.495 and $0.50 respectively). I always find it interesting to see how they react to various news events.

As an aside, I usually get a bit of a traffic spike when I post something on McCain, Obama, or the presidential elections. Unfortunately, it also results in a lot of fevered comments that I have to delete to protect all my many readers' (all three of them) delicate sensibilities.

Of course, if I did it for the traffic, I'd just mention that I have Sarah Palin Bikini pictures.

But that would be wrong. Very, very wrong.

Also, I'm a political junkie, so it's fun to see students in a finance class actually think about politics in a different way.

In any event, it now seems like the McCain for President contract and the Obama contracts have switched places (they're trading at $0.495 and $0.50 respectively). I always find it interesting to see how they react to various news events.

As an aside, I usually get a bit of a traffic spike when I post something on McCain, Obama, or the presidential elections. Unfortunately, it also results in a lot of fevered comments that I have to delete to protect all my many readers' (all three of them) delicate sensibilities.

Of course, if I did it for the traffic, I'd just mention that I have Sarah Palin Bikini pictures.

But that would be wrong. Very, very wrong.

Friday, September 12, 2008

Damn The Data - Full Speed Ahead.

I finally got into heavy data grinding mode for a conference submission that's due on Monday. I should be done with my part of the work and will have tables to show today by 5. My coauthor is working on another paper with a deadline of tomorrow, so he won't even look at this stuff until Friday afternoon at the earliest. The deadline is not until until Monday, so we have time.

To do my part, I had to update the data set to reflect the latest year or so of data. I thought "this should be easy." That thought was four days and about 30 hours of programming ago. It turns out that the final data set resulted from three intermediate steps, which also required data sets to be updated.